Chapter 7 Surplus Production Models

7.1 Introduction

In the previous chapters we have used and fitted what we have called static models that are stable through time (e.g. growth models using vB(), Gz(), or mm()). In addition, in the chapters Model Parameter Estimation and On Uncertainty, we have already introduced surplus production models (spm), that can be used to provide a stock assessment (e.g. the Schaefer model) and provide an example of dynamic models that use time-series of data. However, the development of the details of such models has been limited while we have focussed on particular modelling methods. Here we will examine surplus production models in more detail.

Surplus production models (alternatively Biomass Dynamic models; Hilborn and Walters, 1992) pool the overall effects of recruitment, growth, and mortality (all aspects of production) into a single production function dealing with undifferentiated biomass (or numbers). The term “undifferentiated” implies that all aspects of age and size composition, along with gender and other differences, are effectively ignored.

To conduct a formal stock assessment it is necessary, somehow, to model the dynamic behaviour and productivity of an exploited stock. A major component of these dynamics is the manner in which a stock responds to varied fishing pressure through time, that is, by how much does it increase or decrease in size. By studying the effects of different levels of fishing intensity it is often possible to assess a stock’s productivity. Surplus production models provide for the simplest stock assessments available that attempt to generate a description of such stock dynamics based on fitting the model to data from the fishery.

In the 1950s, Schaefer (1954, 1957) described how to use surplus production models to generate a fishery’s stock assessment. They have been developed in many ways since (Hilborn and Walters, 1992; Prager, 1994; Haddon, 2011; Winker et al, 2018) and it is a rapid survey of these more recent dynamic models that we will consider here.

7.1.1 Data Needs

The minimum data needed to estimate parameters for modern discrete versions of such models are at least one time-series of an index of relative abundance and an associated time-series of catch data. The catch data can cover more years than the index data. The index of relative stock abundance used in such simple models is often catch-per-unit-effort (cpue) but could be some fishery-independent abundance index (e.g., from trawl surveys, acoustic surveys), or both could be used.

7.1.2 The Need for Contrast

Despite occasional more recent use (Elder, 1979; Saila et al, 1979; Punt, 1994; Haddon, 1998), the use of surplus production models appears to have gone out of fashion in the 1980s. This was possibly because early on in their development it was necessary to assume the stocks being assessed were in equilibrium (Elder, 1979; Saila et al, 1979), and this often led to overly optimistic conclusions that were not supportable in the longer term. Hilborn (1979) analyzed many such situations and demonstrated that the data used were often too homogeneous; they lacked contrast in their effort levels and hence were uninformative about the dynamics of the populations concerned. For the data to lack contrast means that fishing catch and effort information is only available for a limited range of stock abundance levels and limited fishing intensity levels. A limited effort range means the range of responses to different fishing intensity levels will also be limited. A lack of such contrast can also arise when the stock dynamics are driven more by environmental factors than by the catches so that the stock can appear to respond to the fishery in unexpected ways (e.g. large changes to the stock despite no changes in catch or effort).

A strong assumption made with surplus production models is that the measure of relative abundance used provides an informative index of the relative stock abundance through time. Generally, the assumption is that there is a linear relationship between stock abundance and cpue, or other indices (though this is not necessarily a 1:1 relationship). The obvious risk is that this assumption is either false or can be modified depending on conditions. It is possible that cpue, for example, may become hyper-stable, which means it does not change even when a stock declines or increases. Or the variation of the index may increase so much as a result of external influences that detection of an abundance trend becomes impossible. For example, very large changes in cpue between years may be observed but not be biologically possible given the productivity of a stock (Haddon, 2018).

A different but related assumption is that the quality of the effort and subsequent catch-rates remains the same through time. Unfortunately, the notion of ‘effort creep’ as a result of technological changes in fishing gear, changes in fishing behaviour or methods, or other changes in fishing efficiency, is invariably a challenge or problem for assessments that rely on cpue as an index of relative abundance. The notion of effort-creep implies that the effectiveness of effort increases so that any observed nominal cpue, based on nominal effort, will over-estimate the relative stock abundance (it is biased high). Statistical standardization of cpue (Kimura, 1981; Haddon, 2018) can address some of these concerns but obviously can only account for factors for which data is available. For example, if one introduces GPS plotters or colour echo-sounders into a fishery, which would tend to increase the effectiveness of effort, but have no record of which vessels introduced them and when, their positive influence on catch rates would not be able to be accounted for by standardization.

7.1.3 When are Catch-Rates Informative

A possible test of whether the assumed relationship between abundance and any index of relative abundance is real and informative can be derived from the implication that, in a developed fishery, if catches are allowed to increase then it is expected that cpue will begin to decline some time after. Similarly, if catches are reduced to be less than surplus production, perhaps through management or marketing changes, then cpue would be expected to increase some time soon after as stock size increases. The idea being that if catches are less than the current productivity of a stock then eventually the stock size and thereby cpue should increase and vice-versa. If catches declined through a lack of availability but stayed at or above the current productivity then, of course, the cpue could not increase and may even decline further despite, perhaps minor, reductions in catch. Emphasis was placed upon developed fisheries because when a fishery begins, any initial depletion of the biomass will lead to “windfall” catches (MacCall, 2009) as the stock is fished down, which in turn will lead to cpue levels that would not be able to be maintained once a stock has been reduced away from unfished levels.

The expectation is, therefore, that in a developed fishery cpue would be, in many cases, negatively correlated with catches, possibly with a time-lag between cpue changing in response to changes in catches. If we can find such a relationship this usually means there is some degree of contrast in the data, if we cannot find such a negative relationship this generally means the information content of the data, with regard to how the stock responds to the fishery, is too low to inform an assessment based only on catches and the index of relative abundance. That is, the cpue adds little more information that that available in the catches.

We will use the MQMF data-set schaef to illustrate these ideas. schaef contains the catches and cpue of the original yellow-fin tuna data from Schaefer (1957), which was an early example of the use of surplus production models to conduct stock assessments.

| year | catch | effort | cpue | year | catch | effort | cpue |

|---|---|---|---|---|---|---|---|

| 1934 | 60913 | 5879 | 10.3611 | 1945 | 89194 | 9377 | 9.5120 |

| 1935 | 72294 | 6295 | 11.4844 | 1946 | 129701 | 13958 | 9.2922 |

| 1936 | 78353 | 6771 | 11.5719 | 1947 | 160134 | 20381 | 7.8570 |

| 1937 | 91522 | 8233 | 11.1165 | 1948 | 200340 | 23984 | 8.3531 |

| 1938 | 78288 | 6830 | 11.4624 | 1949 | 192458 | 23013 | 8.3630 |

| 1939 | 110417 | 10488 | 10.5279 | 1950 | 224810 | 31856 | 7.0571 |

| 1940 | 114590 | 10801 | 10.6092 | 1951 | 183685 | 18726 | 9.8091 |

| 1941 | 76841 | 9584 | 8.0176 | 1952 | 192234 | 31529 | 6.0971 |

| 1942 | 41965 | 5961 | 7.0399 | 1953 | 138918 | 36423 | 3.8140 |

| 1943 | 50058 | 5930 | 8.4415 | 1954 | 138623 | 24995 | 5.5460 |

| 1944 | 64094 | 6397 | 10.0194 | 1955 | 140581 | 17806 | 7.8951 |

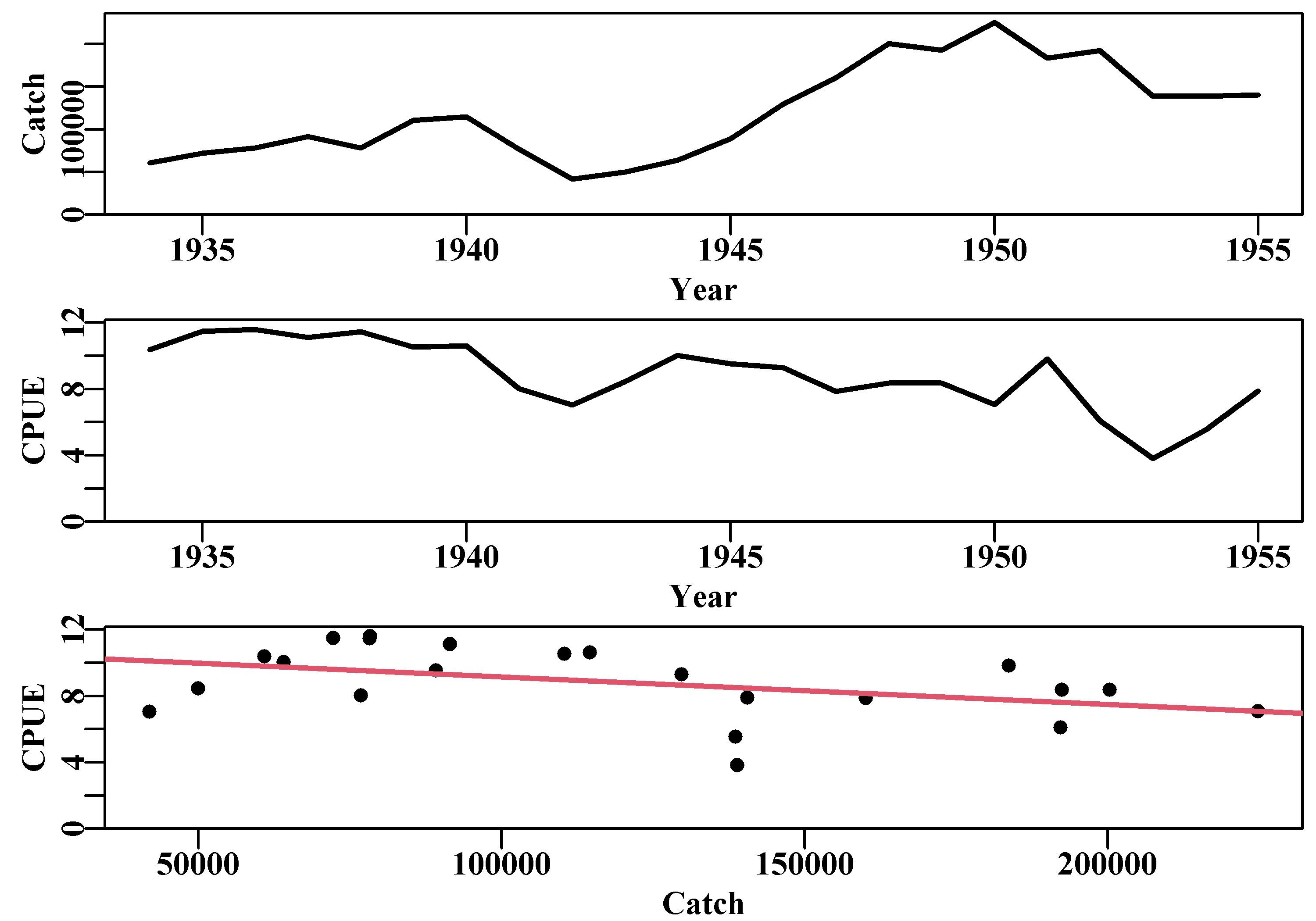

The plot of catch, cpue, and their relationship, Figure(7.1), only exhibits a weak negative relationship between cpue and catch. If we examine the outcome of the regression conducted using lm() by using summary(model), we find this regression is only just significant at P = 0.04575. However, this reflects a correlation with no time-lags, i.e. a lag = 0. We do not know how many years may need to pass before we can detect a potential effect of a change in catch on cpue, so hence, we need to do a time-lagged correlation analysis between cpue and catch; for that we can use the base R cross-correlation function ccf().

#schaef fishery data and regress cpue and catch Fig 7.1

parset(plots=c(3,1),margin=c(0.35,0.4,0.05,0.05))

plot1(schaef[,"year"],schaef[,"catch"],ylab="Catch",xlab="Year",

defpar=FALSE,lwd=2)

plot1(schaef[,"year"],schaef[,"cpue"],ylab="CPUE",xlab="Year",

defpar=FALSE,lwd=2)

plot1(schaef[,"catch"],schaef[,"cpue"],type="p",ylab="CPUE",

xlab="Catch",defpar=FALSE,pch=16,cex=1.0)

model <- lm(schaef[,"cpue"] ~ schaef[,"catch"])

abline(model,lwd=2,col=2) # summary(model)

Figure 7.1: The catches and cpue by year, and their relationship, described by a regression, for the Schaefer (1957) yellowfin tuna fishery data.

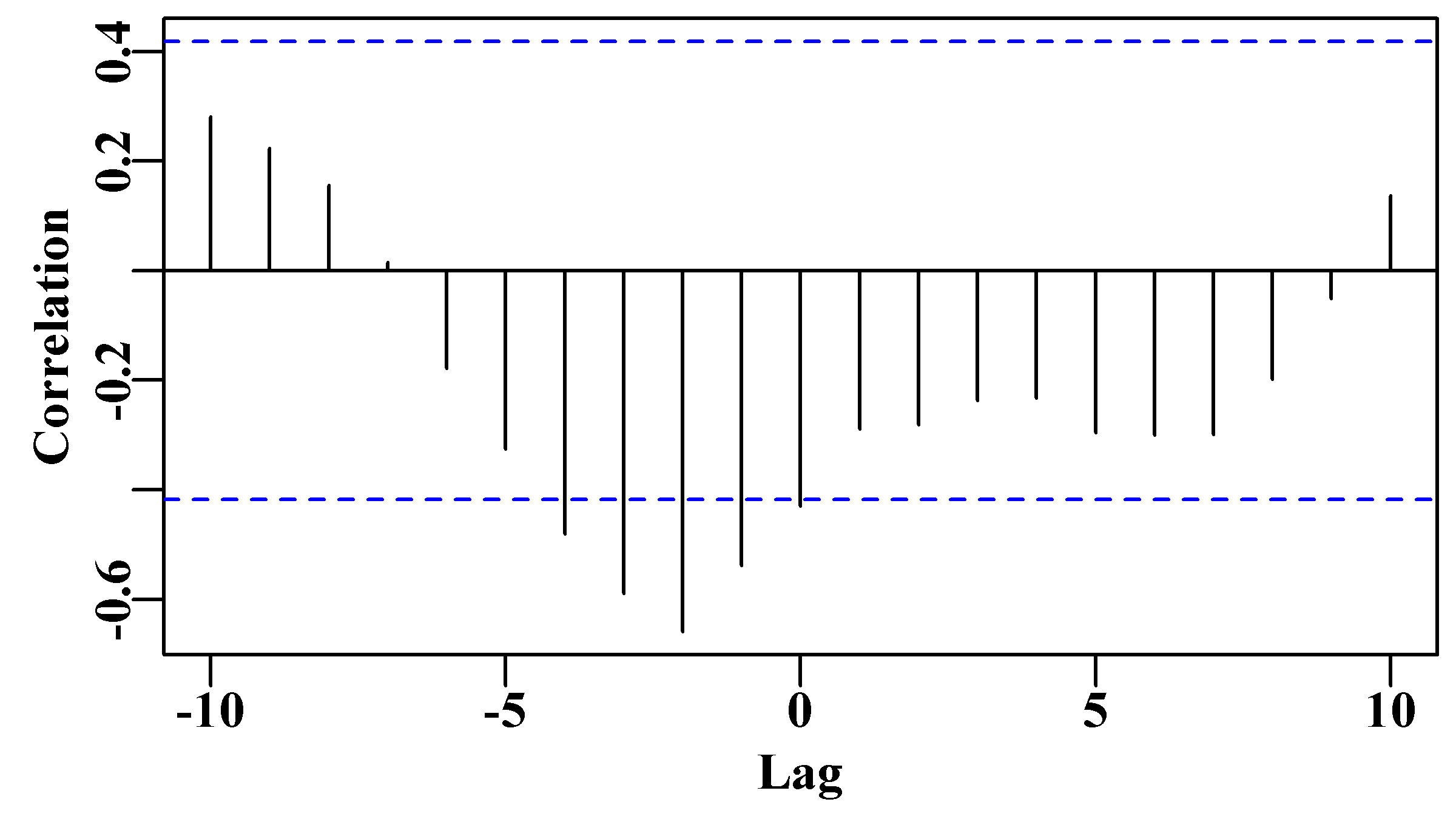

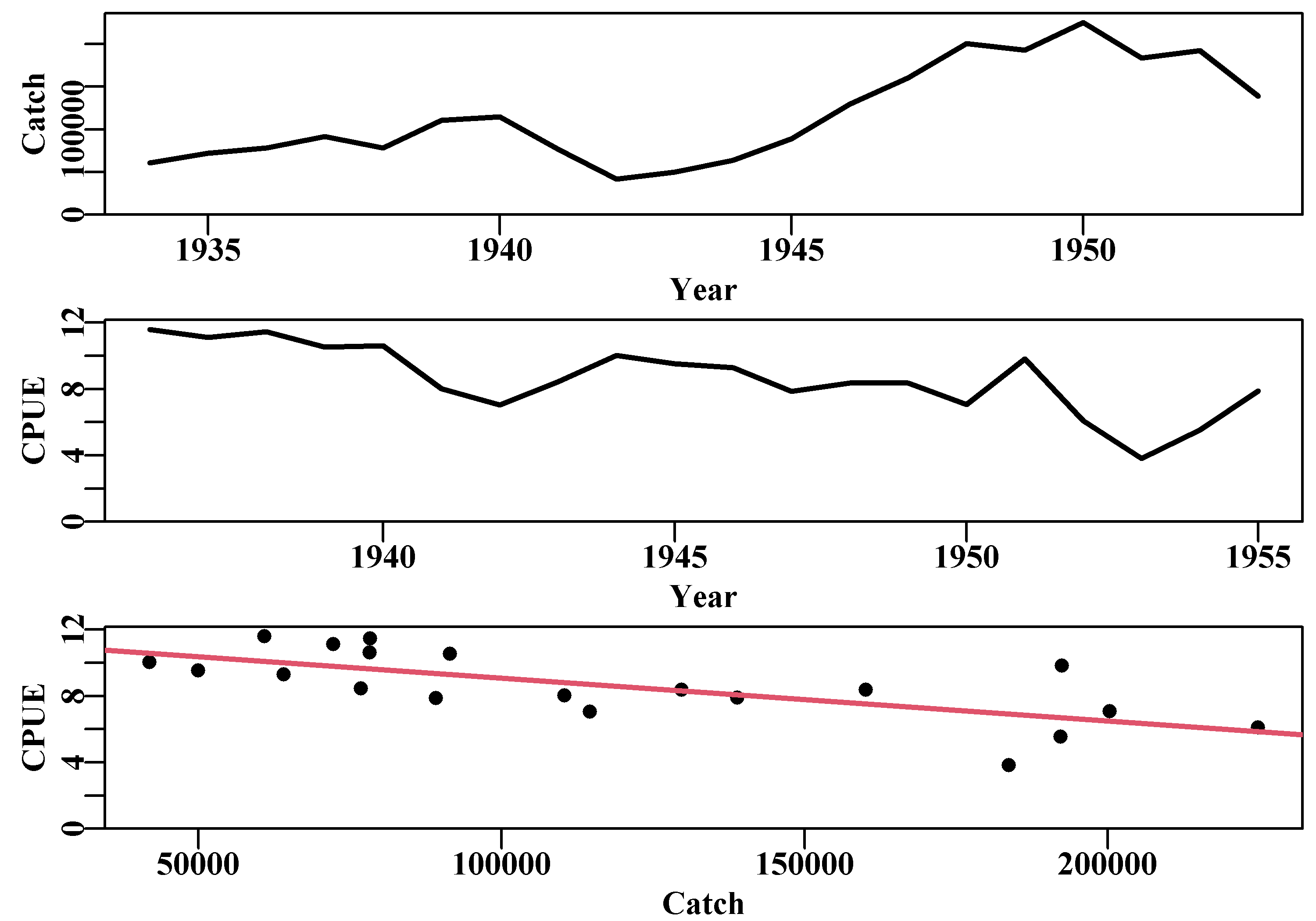

As before there is an indication that a time-lag = 0 is only just significant. However, the significant negative correlation of cpue on catch at a lag of 2 years, Figure(7.2), suggests that there would be sufficient contrast in this yellow-fin tuna data to inform a surplus production model (there are also significant effects at 1, 3, and 4 years). This correlation should become more apparent if we physically lag the CPUE data by two year, Figure(7.3).

#cross correlation between cpue and catch in schaef Fig 7.2

parset(cex=0.85) #sets par parameters for a tidy base graphic

ccf(x=schaef[,"catch"],y=schaef[,"cpue"],type="correlation",

ylab="Correlation",plot=TRUE)

Figure 7.2: The cross correlation between catches and cpue for the Schaefer (1957) yellowfin tuna fishery data (schaef) obtained using the ccf() function in R. The blue dashed lines denote the significant correlation levels.

#now plot schaef data with timelag of 2 years on cpue Fig 7.3

parset(plots=c(3,1),margin=c(0.35,0.4,0.05,0.05))

plot1(schaef[1:20,"year"],schaef[1:20,"catch"],ylab="Catch",

xlab="Year",defpar=FALSE,lwd=2)

plot1(schaef[3:22,"year"],schaef[3:22,"cpue"],ylab="CPUE",

xlab="Year",defpar=FALSE,lwd=2)

plot1(schaef[1:20,"catch"],schaef[3:22,"cpue"],type="p",

ylab="CPUE",xlab="Catch",defpar=FALSE,cex=1.0,pch=16)

model2 <- lm(schaef[3:22,"cpue"] ~ schaef[1:20,"catch"])

abline(model2,lwd=2,col=2)

Figure 7.3: The catches and cpue, and their relationship, for the Schaefer (1957) yellowfin tuna fishery data. With a negative lag of 2 years on the cpue time-series the negative or inverse correlation becomes more apparent.

The relationship between cpue and catches from the Schaefer (1957) yellowfin tuna fishery data with a negative lag of 2 years imposed on the cpue time-series (rows 3:22 against row 1:20). The very small gradient is a reflection of the catches being reported in ’000s of pounds.

#

# Call:

# lm(formula = schaef[3:22, "cpue"] ~ schaef[1:20, "catch"])

#

# Residuals:

# Min 1Q Median 3Q Max

# -3.10208 -0.92239 -0.06399 1.04280 3.11900

#

# Coefficients:

# Estimate Std. Error t value Pr(>|t|)

# (Intercept) 1.165e+01 7.863e-01 14.814 1.59e-11

# schaef[1:20, "catch"] -2.576e-05 6.055e-06 -4.255 0.000477

#

# Residual standard error: 1.495 on 18 degrees of freedom

# Multiple R-squared: 0.5014, Adjusted R-squared: 0.4737

# F-statistic: 18.1 on 1 and 18 DF, p-value: 0.00047657.2 Some Equations

The dynamics of the stock being assessed are described using an index of relative abundance. The index, however it is made, is assumed to reflect the biomass available to the method used to estimate it (fishery-dependent cpue or an independent survey) and this biomass is assumed to be affected by the catches removed by the fishery. This means, if we are using commercial catch-per-unit-effort (cpue), that strictly we are dealing with the exploitable biomass and not the spawning biomass (which is the more usual objective of stock assessments). However, generally, the assumption is made that the selectivity of the fishery is close to the maturity ogive so that the index used is still indexing spawning biomass, at least approximately. Even so, exactly what is being indexed should be considered explicitly before drawing such conclusions.

In general terms, the dynamics are designated as a function of the biomass at the start of a given year t, though it could, by definition, refer to a different date within a year. Remember that the end of a year is effectively the same as the start of the next year although precisely which is used will influence how to start and end the analysis (e.g. from which biomass-year to remove the catches taken in a given year):

\[\begin{equation} \begin{split} {B_0} &= {B_{init}} \\ {B_{t+1}} &= {B_t}+r{B_t}\left( 1-\frac{{B_t}}{K} \right)-{C_t} \end{split} \tag{7.1} \end{equation}\]

where \(B_{init}\) is the initial biomass at whatever time one’s data begins. If data is available from the beginning of fishery then \(B_{init} = K\), where \(K\) is the carrying capacity or unfished biomass. \(B_t\) represents the stock biomass at the start of year \(t\), \(r\) represents the population’s intrinsic growth rate, and \(r{B_t}\left( 1-\frac{{B_t}}{K} \right)\) represents a production function in terms of stock biomass that accounts for recruitment of new individuals, any growth in the biomass of current individuals, natural mortality and assumes linear density-dependent effects on population growth rate. Finally, \(C_t\) is the catch during the year \(t\), which represents fishing mortality. The emphasis placed upon when in the year each term refers to is important, as it determines how the dynamics are modelled in the equations and the consequent R code.

In order to compare and then fit the dynamics of such an assessment model with the real world the model dynamics are also used to generate predicted values for the index of relative abundance in each year:

\[\begin{equation} \hat {I}_{t}=\frac{{C}_{t}}{{E}_{t}}=q{B}_{t} \tag{7.2} \end{equation}\]

where \(\hat {I}_{t}\) is the predicted or estimated mean value of the index of relative abundance in year \(t\), which is compared to the observed indices to fit the model to the data, \(E_t\) is the fishing effort in year \(t\), and \(q\) is the catchability coefficient (defined as the amount of biomass/catch taken with one unit of effort). This relationship also makes the strong assumption that the stock biomass is what is known as a dynamic-pool. This means that irrespective of geographical distance, any influences of the fishery, or the environment, upon the stock dynamics have an effect across the whole stock within each time-step used (often one year but could be less). This is a strong assumption, especially if any consistent spatial structure occurs within a stock or the geographical scale of the fishery is such that large amounts of time would be needed for fish in one region to travel to a different region. Again, awareness of these assumptions is required to appreciate the limitations and appropriately interpret any such analyses.

7.2.1 Production Functions

A number of functional forms have been put forward to describe the productivity of a stock and how it responds to stock size. We will consider two, the Schaefer model and a modified form of the Fox (1970) model, plus a generalization that encompasses both:

The production function of the Schaefer (1954, 1957) model is:

\[\begin{equation} f\left( {B}_{t}\right)=r{B}_{t}\left( 1-\frac{{B}_{t}}{K} \right) \tag{7.3} \end{equation}\]

while a modified version of the Fox (1970) model uses:

\[\begin{equation} f\left( {B_t}\right)=\log({K})r{B}_{t}\left( 1-\frac{\log({B_t})}{\log({K})}\right) \tag{7.4} \end{equation}\]

The modification entails the inclusion of the \(\log(K)\) as the first term, which only acts to maintain the maximum productivity at approximately the equivalent of a similar set of parameters in the Schaefer model.

Pella and Tomlinson (1969) produced a generalized production function that included the equivalent to both the Schaefer and the Fox model as special cases. Here, we will use an alternative to their formulation that was produced by Polacheck et al (1993). This provides a general equation for the population dynamics that can be used for both the Schaefer and the Fox model, and gradations between, depending on the value of a single parameter p.

\[\begin{equation} {B}_{t+1}={B}_{t}+{rB_t}\frac{1}{p}\left( 1- \left(\frac{{B}_{t}}{K} \right)^p \right)-{{C}_{t}} \tag{7.5} \end{equation}\]

where the first term, \(B_t\), is the stock biomass at time \(t\), and the last term is

\(C_t\), which is the catch taken in time \(t\). The middle term is a more complex component that defines the production curve. This is made up of \(r\), the intrinsic rate of population growth, \(B_t\), the current biomass at time \(t\), \(K\), the carrying capacity or maximum population size, and \(p\) is a term that controls any asymmetry of the production curve. If \(p\) is set to 1.0 (the default in the MQMF discretelogistic() function), this equation simplifies to the classical Schaefer model (Schaefer, 1954, 1957). Polacheck et al (1993) introduced the equation above, but it tends to be called the Pella-Tomlinson (1969) surplus production model (though their formulation was different it has very similar properties).

The sub-term \(rB_{t}\) represents unconstrained exponential population growth (because in this difference equation, it is added to \(B_t\)), which, as long as \(r > 0.0\), would lead to unending positive population growth in the absence of catches (such positive exponential growth is still exemplified by the world’s human population; although plague in the 14th century reversed that trend for a brief but particularly unhappy time). The sub-term \((1/p)(1 – (Bt/K)^p)\) provides a constraint on the exponential growth term because its value tends to zero as the population size increases. This acts as, and is known as, a density-dependent effect.

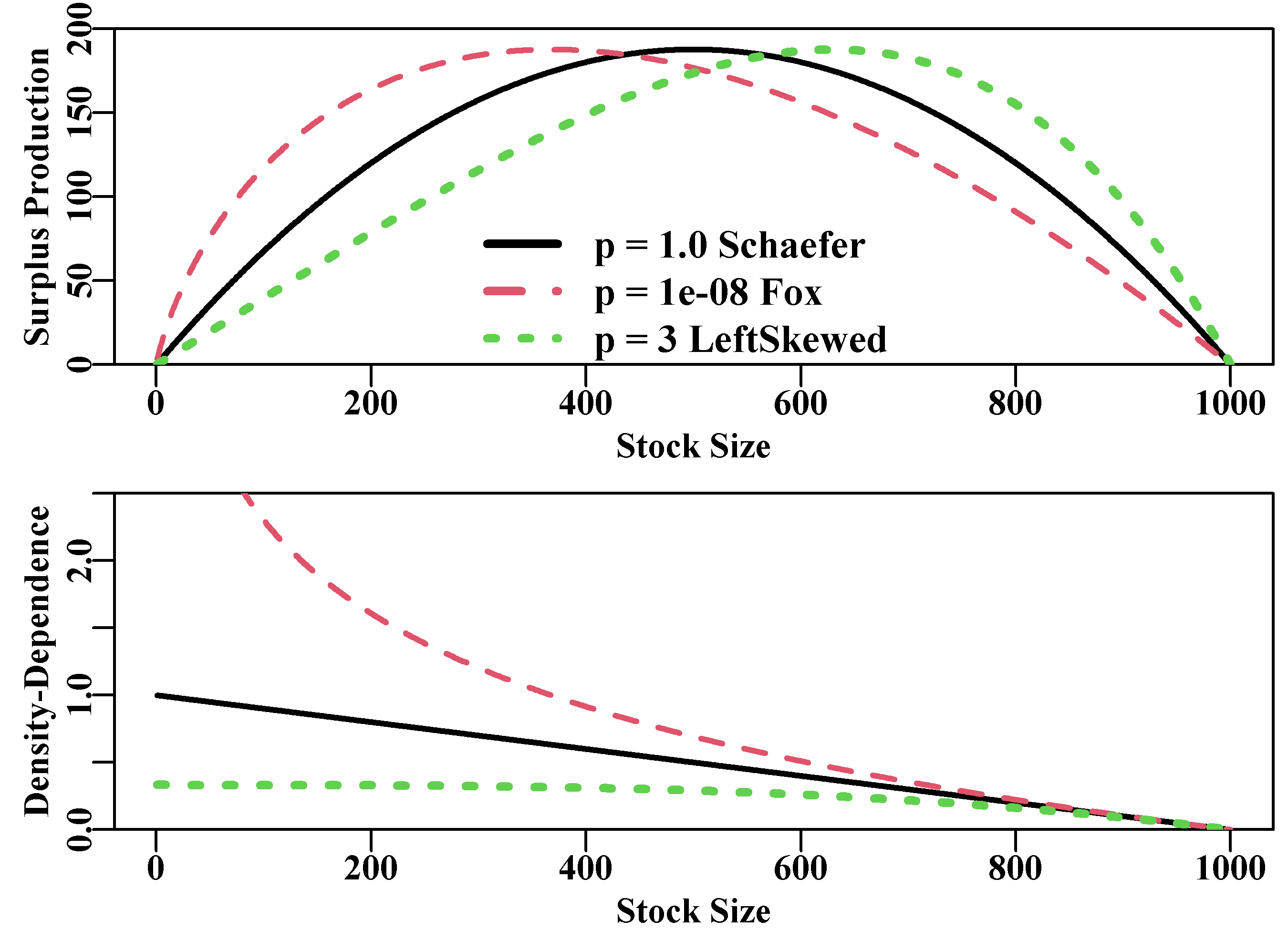

When p is set to 1.0 this equation becomes the same as the Schaefer model (linear density-dependence). But when p is set to a very small number, say 1e-08, then the formulation becomes equivalent to the Fox model’s dynamics. Values of p > 1.0 lead to a production curve skewed to the left with the mode to the right of center. With p either > 1 or < 1, the density-dependence would no longer be linear in character. Generally, one would fix the p value and not attempt to fit it using data. Catch and an index of relative abundance alone would generally be insufficient to estimate the detailed effect on productivity of relative population size.

#plot productivity and density-dependence functions Fig7.4

prodfun <- function(r,Bt,K,p) return((r*Bt/p)*(1-(Bt/K)^p))

densdep <- function(Bt,K,p) return((1/p)*(1-(Bt/K)^p))

r <- 0.75; K <- 1000.0; Bt <- 1:1000

sp <- prodfun(r,Bt,K,1.0) # Schaefer equivalent

sp0 <- prodfun(r,Bt,K,p=1e-08) # Fox equivalent

sp3 <- prodfun(r,Bt,K,3) #left skewed production, marine mammal?

parset(plots=c(2,1),margin=c(0.35,0.4,0.1,0.05))

plot1(Bt,sp,type="l",lwd=2,xlab="Stock Size",

ylab="Surplus Production",maxy=200,defpar=FALSE)

lines(Bt,sp0 * (max(sp)/max(sp0)),lwd=2,col=2,lty=2) # rescale

lines(Bt,sp3*(max(sp)/max(sp3)),lwd=3,col=3,lty=3) # production

legend(275,100,cex=1.1,lty=1:3,c("p = 1.0 Schaefer","p = 1e-08 Fox",

"p = 3 LeftSkewed"),col=c(1,2,3),lwd=3,bty="n")

plot1(Bt,densdep(Bt,K,p=1),xlab="Stock Size",defpar=FALSE,

ylab="Density-Dependence",maxy=2.5,lwd=2)

lines(Bt,densdep(Bt,K,1e-08),lwd=2,col=2,lty=2)

lines(Bt,densdep(Bt,K,3),lwd=3,col=3,lty=3)

Figure 7.4: The effect of the p parameter on the Polacheck et al, 1993, production function (upper plot) and on the density-dependent term (lower plot). Note the rescaling of the productivity to match that produced by the Schaefer curve. Stock size could be biomass or numbers.

The Schaefer model assumes a symmetrical production curve with maximum surplus production or maximum sustainable yield (MSY) at \(0.5K\) and the density-dependent term trends linearly from 1.0 at very low population sizes to zero as \(B_t\) tends towards \(K\). The Fox model is approximated when p has a small value, say \(p=1e-08\), which generates an asymmetrical production curve with the maximum production at some lower level of depletion (in this case at \(0.368K\), found using Bt[which.max(sp0)]). The density-dependent term is non-linear and the maximum productivity (\(MSY\)) occurs where the density-dependent term = 1.0. Without the re-scaling used in Figure(7.4) the Fox model is generally more productive than the Schaefer as a result of the density-dependent term becoming greater than 1.0 at stock sizes less than \(B_{MSY}\), the stock biomass that generates \(MSY\). With values of p > 1.0, the maximum productivity occurs at higher stock sizes and with population growth rates increasing only almost linearly at lower stock sizes and density-dependent declines only occurring at rather higher stock levels. Such dynamics would be more typical of marine mammals than of fish.

The Schaefer model can be regarded as more conservative than the Fox in that it requires the stock size to be higher for maximum production and generally leads to somewhat lower levels of catch, though exceptions could occur because of the generally higher productivity from Fox-type models.

7.2.2 The Schaefer Model

For the Schaefer model we would set \(p = 1.0\) leading to:

\[\begin{equation} {B}_{t+1}={B}_{t}+r{B}_{t}\left( 1-\frac{{B}_{t}}{K} \right)-{C}_{t} \tag{7.6} \end{equation}\]

Given a time-series of fisheries data there will always be an initial biomass which might be \(B_{init} = K\), or \(B_{init}\) being some fraction of \(K\), depending on whether the stock was deemed to be depleted when data from the fishery first became available. It is also not impossible that \(B_{init}\) can be larger than \(K\), as real populations tend not to exhibit a stable equilibrium.

Fitting the model to data would require at least three parameters, the \(r\), the \(K\), and the catchability coefficient \(q\) (\(B_{init}\) might also be needed). However, it is possible to use what is known as a “closed-form” method for estimating the catchability coefficient \(q\):

\[\begin{equation} \hat{q}=\exp \left( \frac{1}{n}\sum{\log{\left( \frac{{I}_{t}}{\hat{B}_{t}} \right)}} \right) \tag{7.7} \end{equation}\]

which is the back-transformed geometric mean of the observed CPUE divided by the predicted exploitable biomass (Polacheck et al, 1993). This generates an average catchability for the time-series. In circumstances where a fishery has undergone a major change such that the quality of the CPUE has changed, it is possible to have different estimates of catchability for different parts of the time-series. However, care is needed to have a strong defense for such suggested model specifications, especially as the shorter the time-series used to estimate \(q\) the more uncertainty will be associated with it.

7.2.3 Sum of Squared Residuals

Such a model can be fitted using least squares or, more properly, the sum of squared residual errors:

\[\begin{equation} ssq=\sum{\left( \log({I}_{t}) - \log(\hat{I}_{t}) \right)}^{2} \tag{7.8} \end{equation}\]

the log-transformations are required as generally CPUE tends to be distributed log-normally and the least-squares method implies normal random errors. The least squares approach tends to be relatively robust when first searching for a set of parameters that enable a model to fit to available data. However, once close to a solution more modelling options become available if one then uses maximum likelihood methods. The full log-normal log likelihood is:

\[\begin{equation} L\left( data|{B}_{init},r,K,q \right)=\prod\limits_{t}{\frac{1}{{I}_{t}\sqrt{2\pi \hat{\sigma }}}{{e}^{\frac{-\left( \log{{I}_{t}}-\log{{\hat{I_t}}} \right)}{2{{{\hat{\sigma }}}^{2}}}}}} \tag{7.9} \end{equation}\]

Apart from the log transformations this differs from Normal PDF likelihoods by the variable concerned (here \(I_t\)) being inserted before the \(\sqrt{2\pi \hat{\sigma }}\) term. Fortunately, as shown in Model Parameter Estimation, the negative log-likelihood can be simplified (Haddon, 2011), to become:

\[\begin{equation} -veLL=\frac{n}{2}\left( \log(2\pi)+2\log(\hat\sigma)+ 1 \right) \tag{7.10} \end{equation}\]

where the maximum likelihood estimate of the standard deviation, \(\hat\sigma\) is given by:

\[\begin{equation} \hat{\sigma }=\sqrt{\frac{\sum{{{\left( \log({{I}_{t}})-\log( {{\hat{I_t}}}) \right)}^{2}}}}{n}} \tag{7.11} \end{equation}\]

Note the division by n rather than by n-1. Strictly, for the log-normal (in Equ(7.10)), the -veLL should be followed by an additional term:

\[\begin{equation} -\sum{\log({I_t})} \tag{7.12} \end{equation}\]

the sum of the log-transformed observed catch rates. But as this will be constant it is usually omitted. Of course, when using R we can always use the built in probability density function implementations (see negLL() and negLL1()) so such simplifications are not strictly necessary, but they can remain useful when one wishes to speed up the analyses using Rcpp, although Rcpp-syntactic-sugar, which leads to C++ code looking remarkably like R code, now includes versions of dnorm() and related distribution functions.

7.2.4 Estimating Management Statistics

The Maximum Sustainable Yield can be calculated for the Schaefer model simply by using:

\[\begin{equation} MSY=\frac{rK}{4} \tag{7.13} \end{equation}\]

However, for the more general equation using the p parameter from Polacheck et al (1993) one needs to use:

\[\begin{equation} MSY=\frac{rK}{\left(p+1 \right)^\frac{\left(p+1 \right)}{p}} \tag{7.14} \end{equation}\]

which simplifies to Equ(7.13) when \(p = 1.0\). We can use the MQMF function getMSY() to calculate Equ(7.14), which is one illustration of how the Fox model can imply greater productivity than the Schaefer.

#compare Schaefer and Fox MSY estimates for same parameters

param <- c(r=1.1,K=1000.0,Binit=800.0,sigma=0.075)

cat("MSY Schaefer = ",getMSY(param,p=1.0),"\n") # p=1 is default

cat("MSY Fox = ",getMSY(param,p=1e-08),"\n") # MSY Schaefer = 275

# MSY Fox = 404.6674Of course, if you fit the two models to real data this will generally produce different parameters for each and so the derived MSY’s may be closer in value.

It is also possible to produce effort-based management statistics. The effort level that if maintained should lead the stock to achieve MSY at equilibrium is known as \(E_{MSY}\):

\[\begin{equation} E_{MSY} = \frac{r}{q(1+p)} \tag{7.15} \end{equation}\]

which collapses to \(E_{MSY} = r/2q\) for the Schaefer model but remains general for other values of the p parameter. It is also possible to estimate the equilibrium harvest rate (proportion of stock taken each year) that should lead to \(B_{MSY}\), which is the biomass that has a surplus production of MSY:

\[\begin{equation} H_{MSY} = qE_{MSY} = q \frac{r}{q+qp} = \frac{r}{1+p} \tag{7.16} \end{equation}\]

It is not uncommon to see Equ(7.16) depicted as \(F_{MSY} = qE_{MSY}\), but this can be misleading as \(F_{MSY}\) would often be interpreted as an instantaneous fishing mortality rate, whereas, in this case, it is actually a proportional harvest rate. For this reason I have explicitly used \(H_{MSY}\).

7.2.5 The Trouble with Equilibria

The real-world interpretation of management targets is not always straightforward. An equilibrium is now assumed to be unlikely in most fished populations, so the interpretation of MSY is more like an average, long-term expected potential yield if the stock is fished optimally; a dynamic equilibrium might be a better description. The \(E_{MSY}\) is the effort that, if consistently applied, should give rise to the MSY, but only if the stock biomass is at \(B_{MSY}\), the biomass needed to generate the maximum surplus production. Each of these management statistics is derived from equilibrium ideas. Clearly, a fishery could be managed by limiting effort to \(E_{MSY}\), but if the stock biomass starts of badly depleted, then the average long-term yield will not result. In fact, the \(E_{MSY}\) effort level may be too high to permit stock rebuilding in this non-equilibrium world. Similarly, \(H_{MSY}\), would operate as expected but only when the stock biomass was at \(B_{MSY}\). It would be possible to estimate the catch or effort level that should lead the stock to recover to \(B_{MSY}\), and this could be termed \(F_{MSY}\), but this would require conducting stock projections and searching for the catch levels that would eventually lead to the desired result. We will examine making population projections in later sections.

It is important to emphasize that the idea of \(MSY\) and its related statistics are based around the idea of equilibrium, which is a rarity in the real world. At best, a dynamic equilibrium may be achievable but, whatever the case, there are risks associated with the use of such equilibrium statistics. When it was first developed the concept of \(MSY\) was deemed a suitable target towards which to manage a fishery. Now, despite being incorporated into a number of national fisheries acts and laws as the overall objective of fisheries management, it is safer to treat \(MSY\) as an upper limit on fishing mortality (catch); a limit reference point rather than a target reference point.

Ideally, the outcomes from an assessment need to be passed through a harvest control rule (HCR) that provides for formal management advice, with regard to future catches or effort, in response to the estimated stock status (fishing mortality and stock depletion levels). However, few of these potential management outputs are of value without some idea of the uncertainty around their values. As we have indicated, it would also be very useful to be able to project the models into the future to provide a risk assessment of alternative management strategies. But first we need to fit the models to data.

7.3 Model Fitting

Details of the model parameters and other aspects relating to the model can also be found in the help files for each of the functions (try ?spm or ?simpspm). In brief, the model parameters are \(r\) the net population rate of increase (combined individual growth in weight, recruitment, and natural mortality), \(K\) the population carrying capacity or unfished biomass, and \(B_{init}\) is the biomass in the first year. This parameter is only required if the index of relative abundance data (usually cpue ) only becomes available after the fishery has been running for a few years implying that the stock has been depleted to some extent. If no initial depletion is assumed then \(B_{init}\) is not needed in the parameter list and is set equal to \(K\) inside the function. The final parameter is sigma, the standard deviation of the Log-Normal distribution used to describe the residuals. simpspm() and spm() are designed for use with maximum likelihood methods so even if you use ssq() as the criterion of optimum fit, a sigma value is necessary in the parameter vector.

In Australia the index of relative stock abundance is most often catch-per-unit-effort (cpue ), but could be some fishery-independent abundance index (e.g., from trawl surveys, acoustic surveys), or both could be used in one analysis (see simpspmM()). The analysis will permit the production of on-going management advice as well as a determination of stock status.

In this section we will describe the details of how to conduct a surplus production analysis, how to extract the results from that analysis as well as plot out illustrations of those results.

7.3.1 A Possible Workflow for Stock Assessment

When conducting a stock assessment based upon a surplus production model one possible work flow might include:

- read in time-series of catch and relative abundance data. It can help to have functions that check for data completeness, missing values, and other potential issues, but it is even better to know your own data and its limitations.

- use a

ccf()analysis to determine whether the cpue data relative to the catch data may be informative. If a significant negative relation was found this would strengthen any defense of the analysis.

- define/guess a set of initial parameters containing r and K, and optionally \(B_{init}\) = initial biomass, which is used if it is suspected that the fishery data starts after the stock has been somewhat depleted.

- use the function

plotspmmod()to plot up the implications of the assumed initial parameter set for the dynamics. This is useful when searching for plausible initial parameters sets.

- use

nlm()orfitSPM()to search for the optimum parameters once a potentially viable initial parameter set are input. See discussion.

- use

plotspmmod()using the optimum parameters to illustrate the implications of the optimum model and it relative fit (especially using the residual plot).

- ideally one should examine the robustness of the model fit by using multiple different initial parameter sets as starting points for the model fitting procedure, see

robustSPM(). - once satisfied with the robustness of the model fit, use

spmphaseplot()to plot out the phase diagram of biomass against harvest rate so as to determine and illustrate the stock status visually.

- use

spmboot(), asymptotic standard errors, or Bayesian methods from On Uncertainty, to characterize uncertainty in the model fit and outputs. Tabulating and plotting such outputs. See later.

- Document and defend any conclusions reached.

Two common versions of the dynamics are currently available inside MQMF: the classical Schaefer model (Schaefer, 1954) and an approximation to the Fox model (Fox, 1970; Polacheck et al, 1993), both are described in Haddon (2011). Prager (1994) provides many additional forms of analysis that are possible using surplus production models and practical implementations are also provided in Haddon (2011).

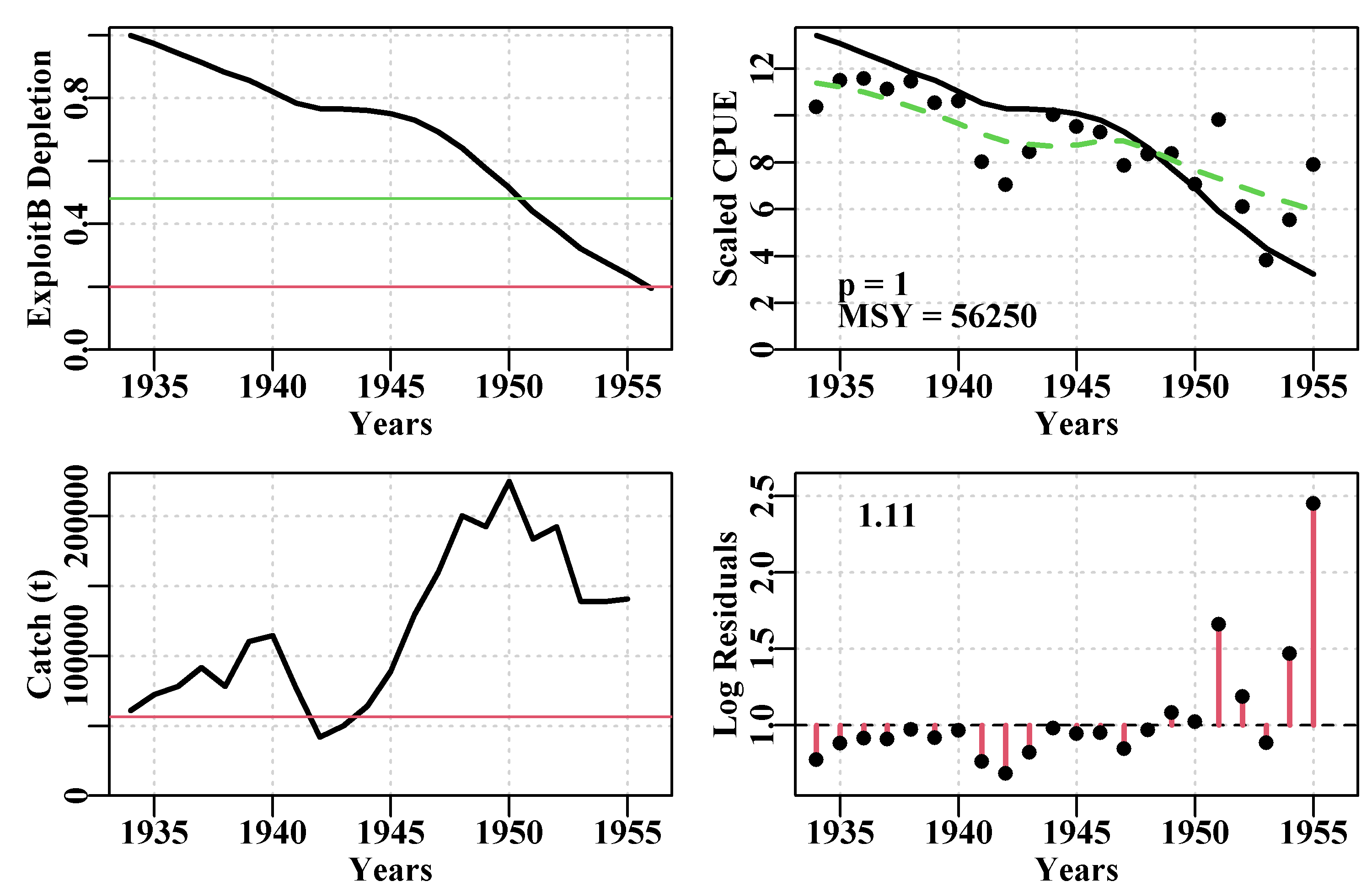

#Initial model 'fit' to the initial parameter guess Fig 7.5

data(schaef); schaef <- as.matrix(schaef)

param <- log(c(r=0.1,K=2250000,Binit=2250000,sigma=0.5))

negatL <- negLL(param,simpspm,schaef,logobs=log(schaef[,"cpue"]))

ans <- plotspmmod(inp=param,indat=schaef,schaefer=TRUE,

addrmse=TRUE,plotprod=FALSE)

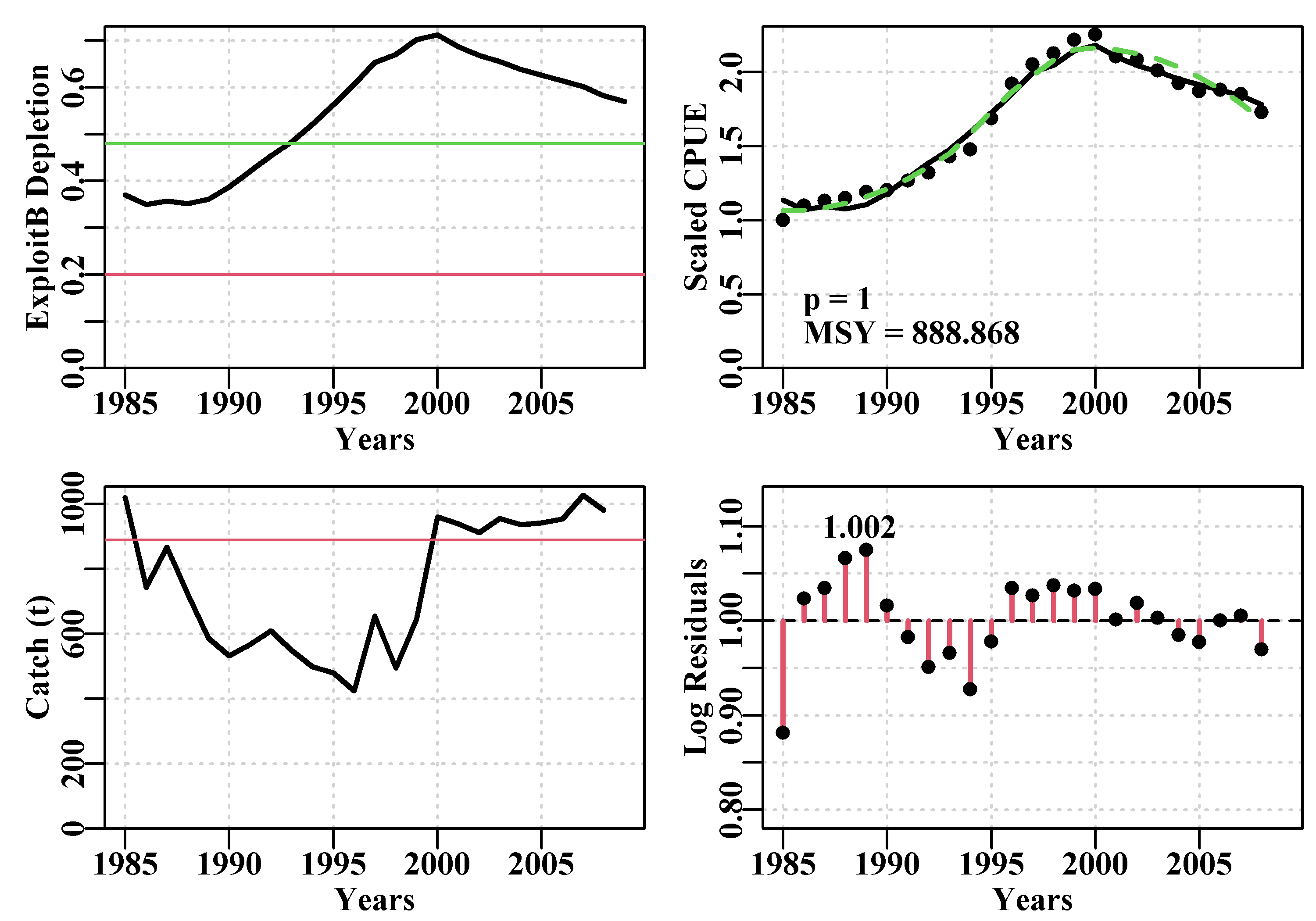

Figure 7.5: The tentative fit of a surplus production model to the schaef data-set using the initial parameter values. The dashed green line in the CPUE plot is a simple loess fit, while the solid line is that implied by the guessed input parameters. The horizontal red line in the catch plot is the predicted MSY. The number in the residual plot is the root mean square error of the log-normal residuals.

The r value of 0.1 leads to a negatL = 8.2877, and a strong residual pattern of all residuals below 1.0 up to about 1950 and four large and positive residuals afterwards. The K value was set at about 10 times the maximum catch and something of that order (10x to 20x) will often lead to sufficient biomass being available that the stock biomass and CPUE trajectories get off the x-axis ready for entry to a minimizer/optimizer. We used the plotprod = FALSE option (the default), as before fitting the model to data there is little point in seeing the predicted productivity curves.

With numerical methods of fitting models to data it is often necessary to take measures to ensure that one obtains a robust, as well as a biologically plausible model fit. One option for robustness is to fit the model twice, with the input parameters for the second fit coming from the first fit. We will use a combination of optim() and nlm() along with negLL1() to estimate the negative log-likelihood during each iteration (this is how fitSPM() is implemented). Within MQMF we have a function spm(), that calculates the full dynamics in terms of predicted changes in biomass, CPUE, depletion, and harvest rate. While this is relatively quick, to speed the iterative model fitting process, rather than use spm(), we use simpspm() to output only the log of the predicted CPUE ready for the minimization, rather than calculate the full dynamics each time. We use simpspm() when we only have a single time-series of an index of relative abundance. If we have more than one index series we should use simpspmM(), spmCE(), and negLLM(); see the help, ?simpspmM, ?spmCE, ?negLLM, and their code to see the implementation in each case. In addition to using simpspmM(), spmCE(), and negLLM() for multiple time-series of indices it is also used to illustrate that model fitting can sometimes generate biologically implausible solutions that are mathematically optimal. As well as putting a penalty penalty0() on the first parameter, \(r\), to prevent it becoming less than 0.0, with the extreme catch history used in the examples to the multi-index functions, depending on the starting parameters, we also need to put a penalty on the annual harvest rates to ensure they stay less than 1.0 (see penalty1(). Biologically it is obviously impossible for there to be more catch than biomass but if we do not constrain the model mathematically, then there is nothing mathematically wrong with having very large harvest rates.

Considerations about speed become more important as the complexity of the models we use increases or we start using computer-intensive methods. None of our parameters should become negative, and they differ greatly in their magnitude, so here we are using natural log-transformed parameters.

#Fit the model first using optim then nlm in sequence

param <- log(c(0.1,2250000,2250000,0.5))

pnams <- c("r","K","Binit","sigma")

best <- optim(par=param,fn=negLL,funk=simpspm,indat=schaef,

logobs=log(schaef[,"cpue"]),method="BFGS")

outfit(best,digits=4,title="Optim",parnames = pnams)

cat("\n")

best2 <- nlm(negLL,best$par,funk=simpspm,indat=schaef,

logobs=log(schaef[,"cpue"]))

outfit(best2,digits=4,title="nlm",parnames = pnams) # optim solution: Optim

# minimum : -7.934055

# iterations : 41 19 iterations, gradient

# code : 0

# par transpar

# r -1.448503 0.2349

# K 14.560701 2106842.7734

# Binit 14.629939 2257885.3255

# sigma -1.779578 0.1687

# message :

#

# nlm solution: nlm

# minimum : -7.934055

# iterations : 2

# code : 2 >1 iterates in tolerance, probably solution

# par gradient transpar

# r -1.448508 6.030001e-04 0.2349

# K 14.560692 -2.007053e-04 2106824.2701

# Binit 14.629939 2.545064e-04 2257884.5480

# sigma -1.779578 -3.688185e-05 0.1687The output from the two-fold application of the numerical optimizers suggests that we did not need to conduct the process twice, but it is precautionary not to be too trustful of numerical methods. By all means do single model fits but do so at your own peril (or perhaps I have had to work with more poor to average quality data than many people!).

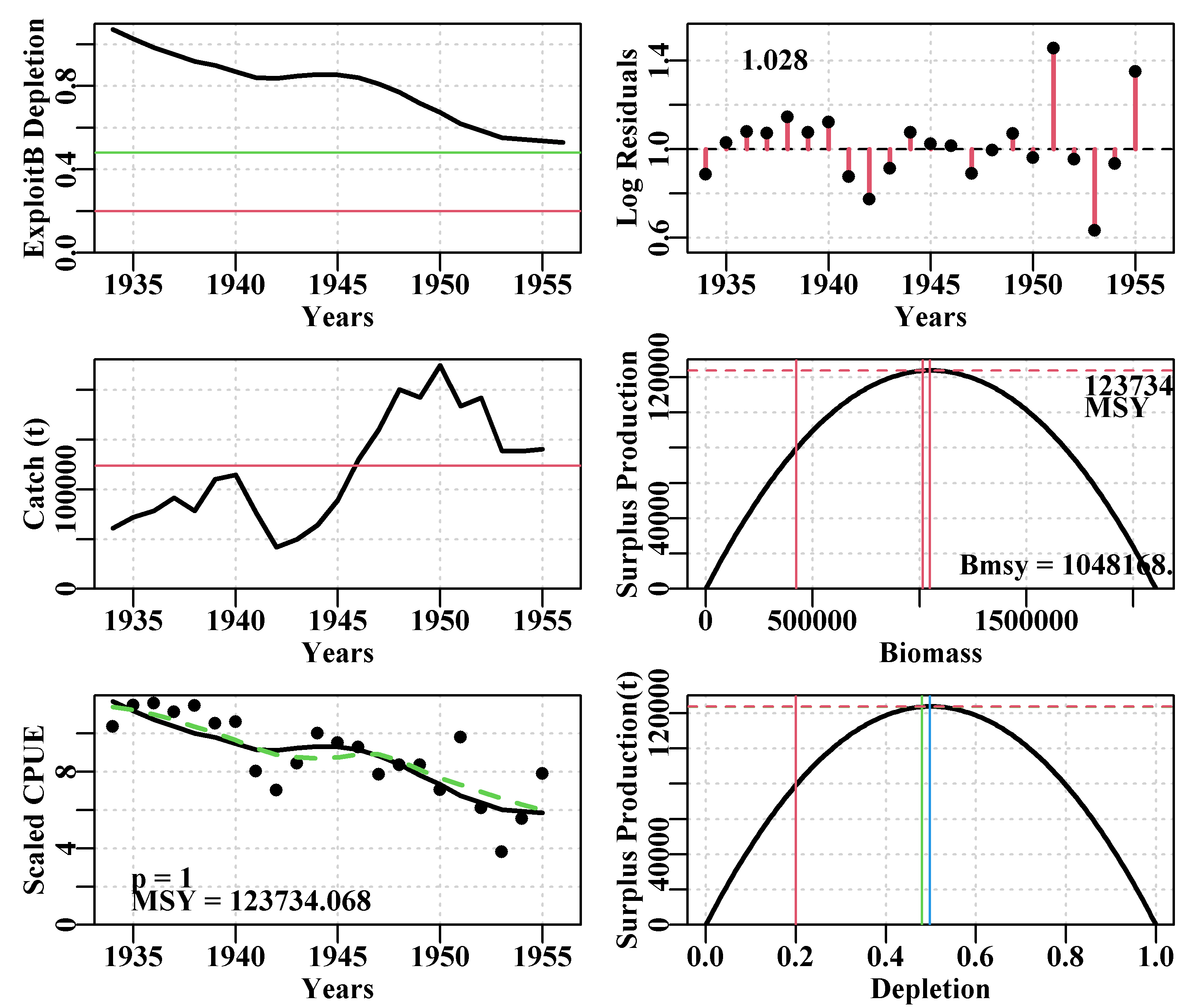

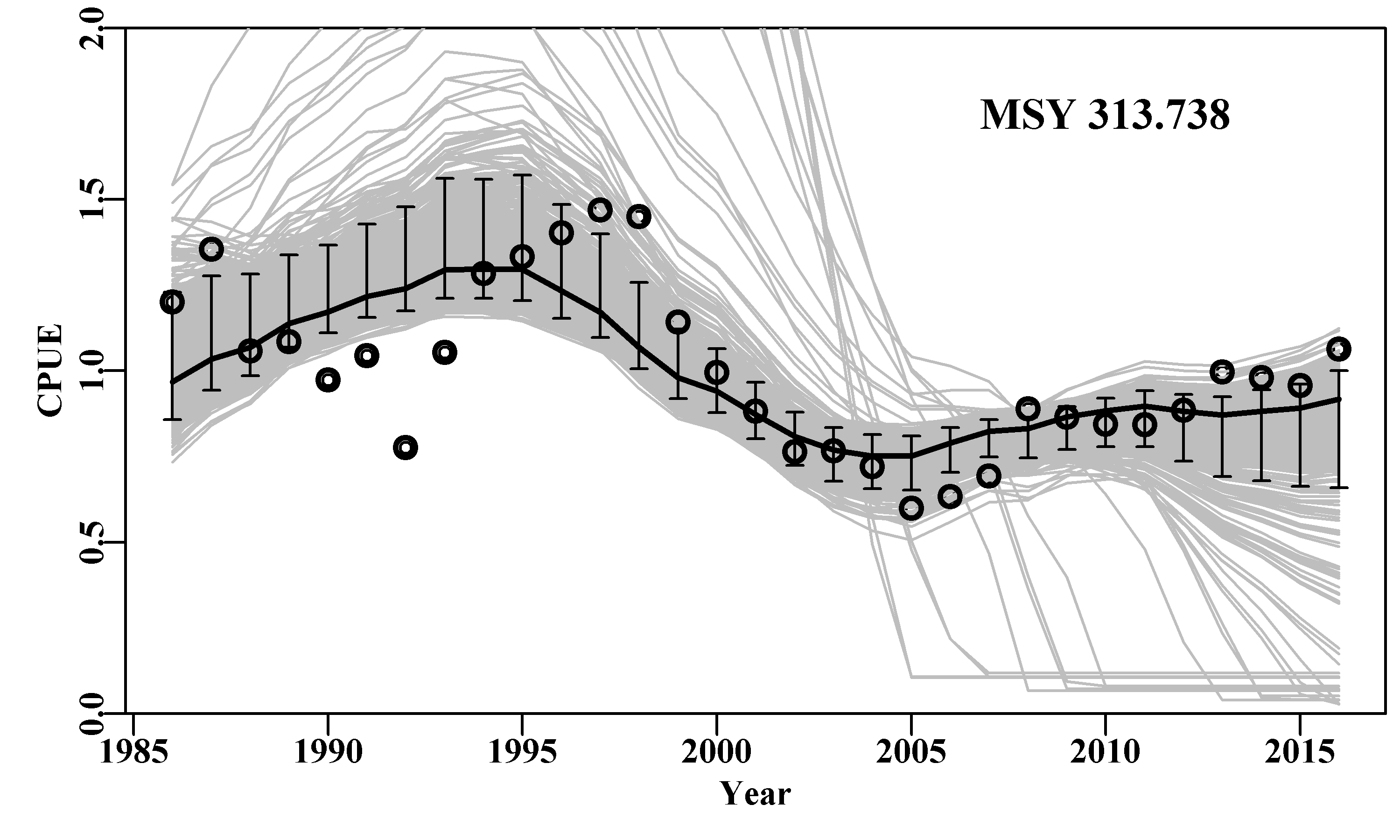

We can now take the optimum parameters from the best2 fit and put them into the plotspmmod() function to visualize the model fit. We now have the optimum parameters so we can include the productivity curves by setting the plotprod argument to TRUE. plotspmmod() does more than just plot the results, it also returns a large list object invisibly so if we want this we need to assign it to a variable or object (in this case ans) in order to use it.

#optimum fit. Defaults used in plotprod and schaefer Fig 7.6

ans <- plotspmmod(inp=best2$estimate,indat=schaef,addrmse=TRUE,

plotprod=TRUE)

Figure 7.6: A summary of the fit of a surplus production model to the schaef data-set given the optimum parameters from the final nlm() fit. In the CPUE plot, the dashed green line is the simple loess curve fit while the solid red line is the optimal model fit.

The object returned by plotspmmod() is a list of objects containing a collection of results, including the optimum parameters, a matrix (ans$Dynamics$outmat) containing the predicted optimal dynamics, the production curve, and numerous summary results. Once assigned to a particular object in the working environment these can be quickly extracted for use in other functions. Try running str() without the max.level=1 argument or set it = 2, to see more details. Lots of functions generate large, informative objects, you should become familiar with exploring them to make sure you understand what is being produces within different analyses.

#the high-level structure of ans; try str(ans$Dynamics)

str(ans, width=65, strict.width="cut",max.level=1) # List of 12

# $ Dynamics :List of 5

# $ BiomProd : num [1:200, 1:2] 100 10687 21273 31860 42446 ...

# ..- attr(*, "dimnames")=List of 2

# $ rmseresid: num 1.03

# $ MSY : num 123731

# $ Bmsy : num 1048169

# $ Dmsy : num 0.498

# $ Blim : num 423562

# $ Btarg : num 1016409

# $ Ctarg : num 123581

# $ Dcurr : Named num 0.528

# ..- attr(*, "names")= chr "1956"

# $ rmse :List of 1

# $ sigma : num 0.169There are also a few MQMF functions to assist with pulling out such results or that use the results from plotspmmod() (see summspm() and spmphaseplot()), which is why the function includes the argument plotout = TRUE, so that a plot need not be produced. However, in many cases it can be simpler just to point to the desired object within the high level object (in this case ans). Notice that the \(MSY\) obtained from the generated productivity curve differs by a small amount from that calculated from the optimal parameters. This is because the productivity curve is obtained numerically by calculating the productivity for a vector of different biomass levels. Its resolution is thus limited by the steps used to generate the biomass vector. Its estimate will invariably be slightly smaller than the parameter derived value.

#compare the parameteric MSY with the numerical MSY

round(ans$Dynamics$sumout,3)

cat("\n Productivity Statistics \n")

summspm(ans) # the q parameter needs more significantr digits # msy p FinalDepl InitDepl FinalB

# 123734.068 1.000 0.528 1.072 1113328.480

#

# Productivity Statistics

# Index Statistic

# q 1 0.0000

# MSY 2 123731.0026

# Bmsy 3 1048168.8580

# Dmsy 4 0.4975

# Blim 5 423562.1648

# Btarg 6 1016409.1956

# Ctarg 7 123581.3940

# Dcurr 8 0.5284Finally, to simplify the future use of this double model fitting process there is an MQMF function, fitSPM() that implements the procedure. You can either use that (check out its code, etc), or repeat the contents of the raw code whichever you find most convenient.

7.3.2 Is the Analysis Robust?

Despite my dire warnings you may be wondering why we bothered to fit the model twice, with the starting point for the second fit being the estimated optimum from the first. One should always remember that we are using numerical methods when we fit these models. Such methods are not fool-proof and can discover false minima. If there are any interactions or correlations between the model parameters then slightly different combinations can lead to very similar values of negative log-likelihood. The optimum model fit still exhibits three relative large residuals towards the end of the time-series of cpue, Figure(7.6). They do not exhibit any particular pattern so we assume they only represent uncertainty, which should make one question how good a model fit one has and how reliable the output statistics are from the analysis. One way we can examine the robustness of the model fit is by examining the influence of the initial model parameters on that model fit.

One implementation of a robustness test uses the robustSPM() MQMF function. This generates \(N\) random starting values by using the optimum log-scale parameter values as the respective mean values of some normal random variables with their respective standard deviation values obtained by dividing those mean values by the scaler argument value (see the code and help of robustSPM() for the full details). The object output from robustSPM() includes the \(N\) vectors of randomly varying initial parameter values, which permits their variation to be illustrated and characterized. Of course, as a divisor, the smaller the scaler value the more variable the initial parameter vectors are likely to be and the more often one might expect the model fitting to fail to find the minimum.

#conduct a robustness test on the Schaefer model fit

data(schaef); schaef <- as.matrix(schaef); reps <- 12

param <- log(c(r=0.15,K=2250000,Binit=2250000,sigma=0.5))

ansS <- fitSPM(pars=param,fish=schaef,schaefer=TRUE, #use

maxiter=1000,funk=simpspm,funkone=FALSE) #fitSPM

#getseed() #generates random seed for repeatable results

set.seed(777852) #sets random number generator with a known seed

robout <- robustSPM(inpar=ansS$estimate,fish=schaef,N=reps,

scaler=40,verbose=FALSE,schaefer=TRUE,

funk=simpspm,funkone=FALSE)

#use str(robout) to see the components included in the output By using the set.seed function the outcome of the pseudo-random numbers used to generate the scattered initial parameter vectors are repeatable. In Table(7.2) we can see that out of 12 trials we obtained 12 with the same final negative log-likelihood to five decimal places, although there was some slight variation apparent in the actual \(r\), \(K\), and \(B_{init}\) values and that led to minor variation in the estimated \(MSY\) values. If we increase the number of trials we finally see some that differ slightly from the optimum.

| ir | iK | iBinit | isigma | iLike | |

|---|---|---|---|---|---|

| 6 | 0.232 | 2521208 | 2394188 | 0.1727 | -5.765 |

| 10 | 0.242 | 2564306 | 1386181 | 0.1659 | 14.306 |

| 11 | 0.237 | 2189281 | 2032237 | 0.1811 | -7.025 |

| 1 | 0.239 | 2351319 | 3401753 | 0.1692 | -6.351 |

| 8 | 0.244 | 2201215 | 2934055 | 0.1795 | -7.078 |

| 3 | 0.233 | 3164529 | 1632687 | 0.1702 | 22.093 |

| 4 | 0.233 | 3482370 | 1584633 | 0.1683 | 34.534 |

| 12 | 0.237 | 3492106 | 1895315 | 0.1653 | 23.789 |

| 2 | 0.247 | 2359029 | 2137751 | 0.1787 | -5.575 |

| 5 | 0.234 | 3057512 | 1502916 | 0.1713 | 23.720 |

| 7 | 0.242 | 1671149 | 2512111 | 0.1687 | 4.228 |

| 9 | 0.230 | 1391893 | 1753155 | 0.1754 | 138.808 |

| r | K | Binit | sigma | -veLL | MSY | |

|---|---|---|---|---|---|---|

| 6 | 0.235 | 2107069 | 2258144 | 0.1687 | -7.93406 | 123725 |

| 10 | 0.235 | 2107034 | 2258103 | 0.1687 | -7.93406 | 123726 |

| 11 | 0.235 | 2107243 | 2258322 | 0.1687 | -7.93406 | 123717 |

| 1 | 0.235 | 2107178 | 2258293 | 0.1687 | -7.93406 | 123722 |

| 8 | 0.235 | 2107119 | 2258218 | 0.1687 | -7.93406 | 123720 |

| 3 | 0.235 | 2107386 | 2258484 | 0.1687 | -7.93406 | 123713 |

| 4 | 0.235 | 2107405 | 2258514 | 0.1687 | -7.93406 | 123713 |

| 12 | 0.235 | 2107417 | 2258533 | 0.1687 | -7.93406 | 123713 |

| 2 | 0.235 | 2106866 | 2257912 | 0.1687 | -7.93406 | 123728 |

| 5 | 0.235 | 2107294 | 2258319 | 0.1687 | -7.93406 | 123713 |

| 7 | 0.235 | 2107319 | 2258401 | 0.1687 | -7.93406 | 123712 |

| 9 | 0.235 | 2106435 | 2257279 | 0.1687 | -7.93406 | 123739 |

Normally one would try more than 12 trials and would examine the effect of the scaler argument. So we will now repeat that analysis 100 times using the same optimum fit and random seed. The table of results output by robustSPM() is sorted by the final -ve log-likelihood but even where this is the same to five decimal places notice there is slight variation in the parameter estimates. This is merely a reflection of using numerical methods.

#Repeat robustness test on fit to schaef data 100 times

set.seed(777854)

robout2 <- robustSPM(inpar=ansS$estimate,fish=schaef,N=100,

scaler=25,verbose=FALSE,schaefer=TRUE,

funk=simpspm,funkone=TRUE,steptol=1e-06)

lastbits <- tail(robout2$results[,6:11],10) | r | K | Binit | sigma | -veLL | MSY | |

|---|---|---|---|---|---|---|

| 12 | 0.23513 | 2105553 | 2256358 | 0.1687 | -7.93405 | 123770 |

| 65 | 0.23513 | 2105553 | 2256358 | 0.1687 | -7.93405 | 123770 |

| 47 | 0.23513 | 2105553 | 2256358 | 0.1687 | -7.93405 | 123770 |

| 11 | 0.23513 | 2105553 | 2256358 | 0.1687 | -7.93405 | 123770 |

| 76 | 0.23513 | 2105553 | 2256358 | 0.1687 | -7.93405 | 123770 |

| 57 | 0.23513 | 2105553 | 2256358 | 0.1687 | -7.93405 | 123770 |

| 23 | 0.23513 | 2105553 | 2256358 | 0.1687 | -7.93405 | 123770 |

| 9 | 0.23513 | 2105553 | 2256358 | 0.1687 | -7.93405 | 123770 |

| 93 | 0.23514 | 2105527 | 2256328 | 0.1687 | -7.93405 | 123771 |

| 55 | 0.23514 | 2105510 | 2256327 | 0.1687 | -7.93405 | 123772 |

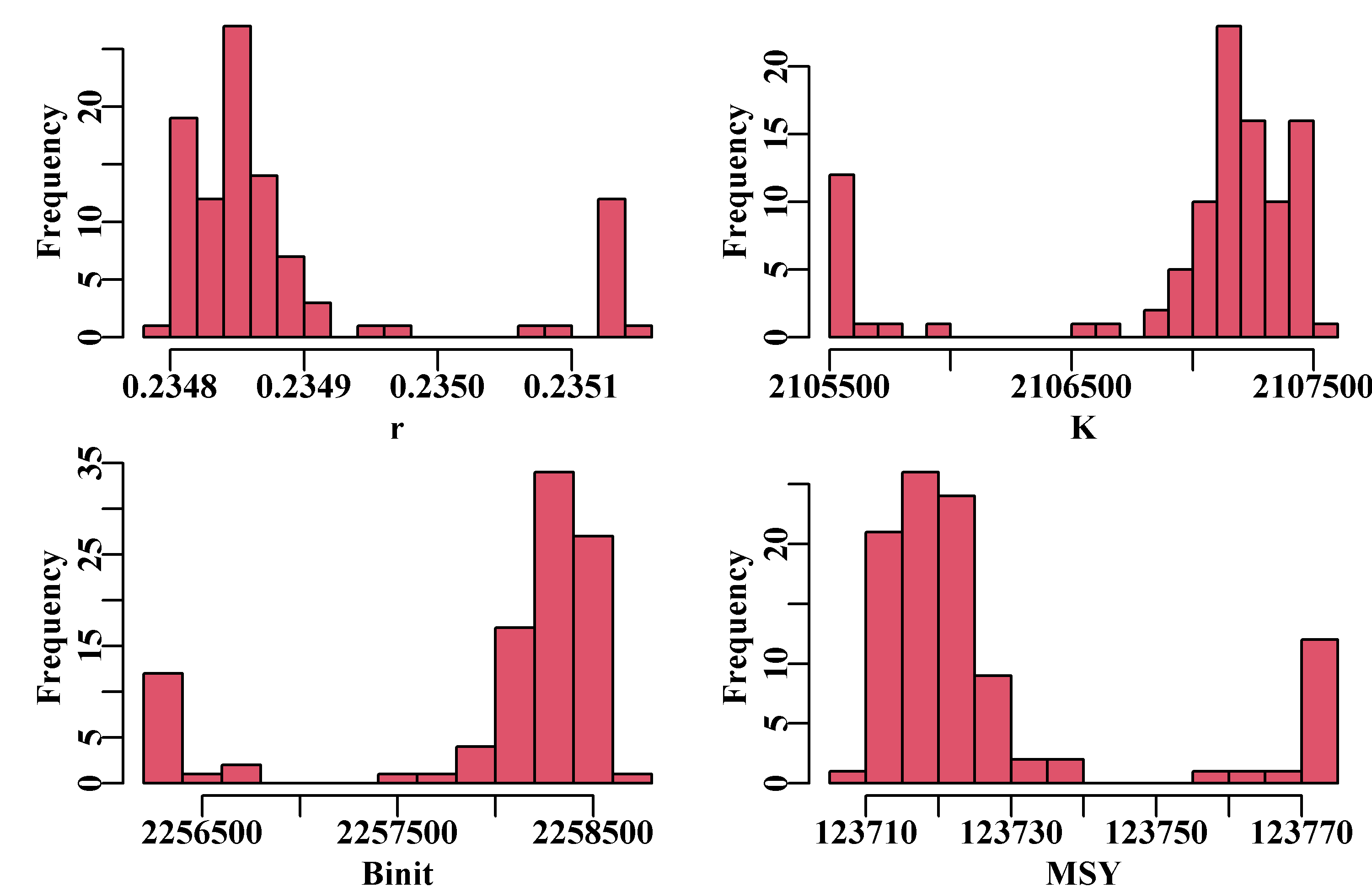

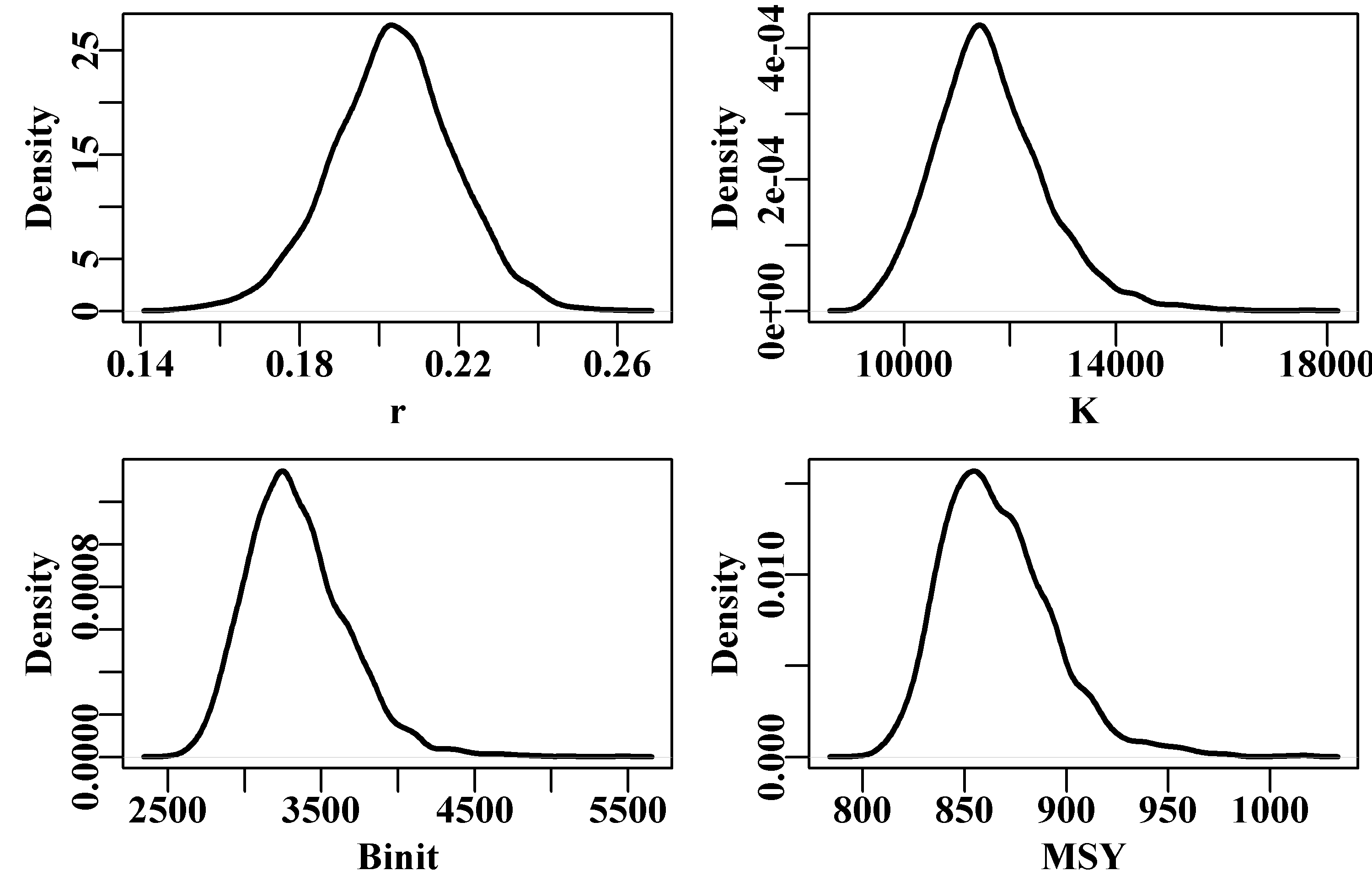

Table(7.3) is only the bottom 10 records of the sorted 100 replicates, and this indicates that all replicates had the same negative log-likelihood (to 5 decimal places). Again, if you look closely at the values given for r, K, Binit, and MSY you will notice differences. If we plot up the final fitted parameter values as distributions, the scale of the variation becomes clear, Figure(7.7).

# replicates from the robustness test Fig 7.7

result <- robout2$results

parset(plots=c(2,2),margin=c(0.35,0.45,0.05,0.05))

hist(result[,"r"],breaks=15,col=2,main="",xlab="r")

hist(result[,"K"],breaks=15,col=2,main="",xlab="K")

hist(result[,"Binit"],breaks=15,col=2,main="",xlab="Binit")

hist(result[,"MSY"],breaks=15,col=2,main="",xlab="MSY")

Figure 7.7: Histograms of the main parameters and MSY from the 100 trials in a robustness test of the model fit to the schaef data-set. The parameter estimates are all close, but still there is variation, which is a reflection of estimation uncertainty. To improve on this, one might try a smaller steptol, which defaults to 1e-06, but stable solutions might not always be possible. If you use steptol = 1e-07 the range of values across the variation becomes much tighter but some slight variation remains, as expected when using numerical methods. This is another reason why the particular values for the parameter estimates are most meaningful when we also have an estimate of variation or of uncertainty.

Even with negative log-likelihood values that are very close in value (to five decimal places), Figure(7.7), there are slight deviations possible from the optimum values that occur most often. This emphasizes the need to examine the uncertainty in the analysis closely. Given that most of the trials lead to the same optimum values the median values across all trials can identify optimum values.

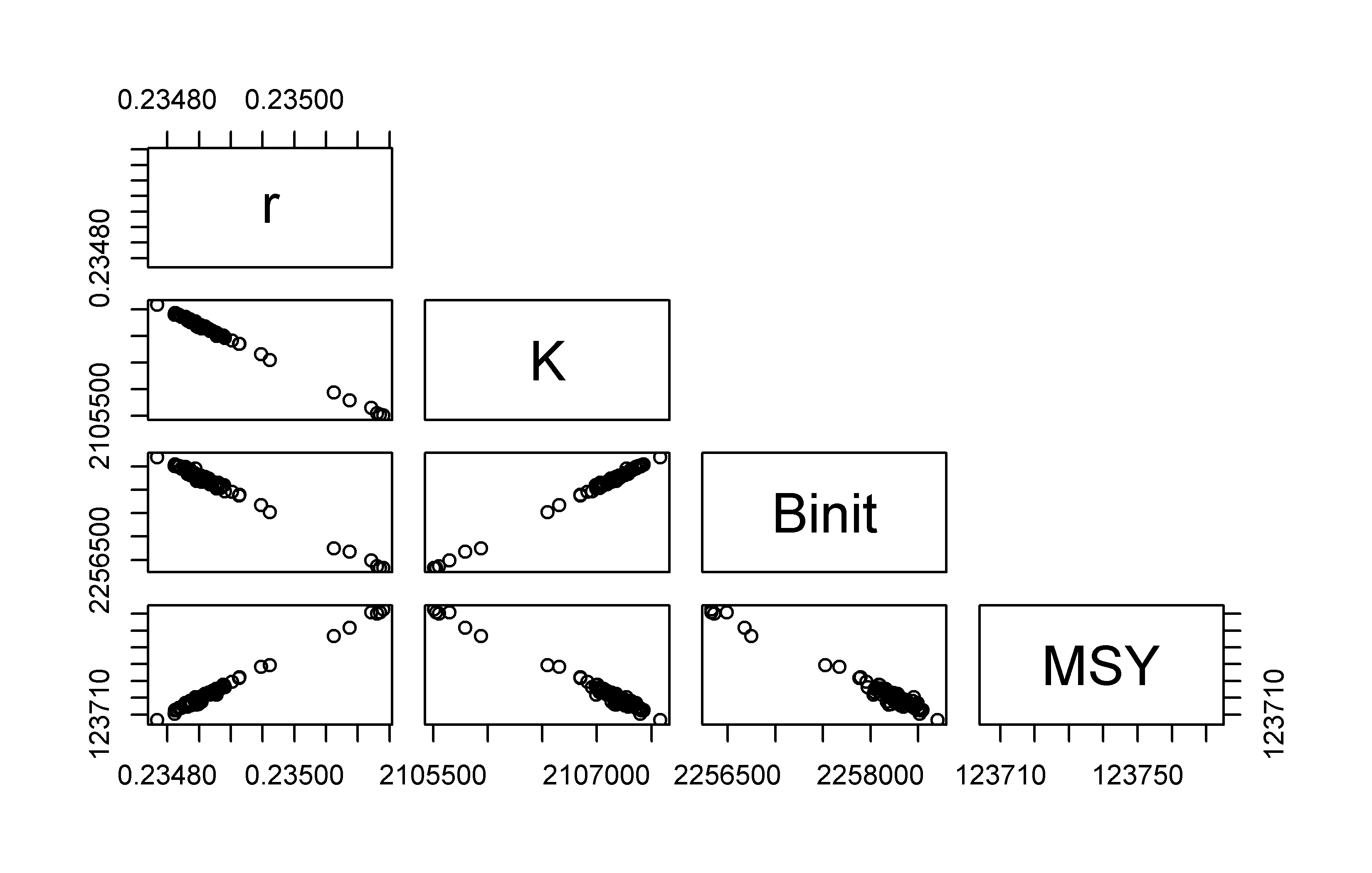

An alternative way of visualizing the final variation in parameter estimates from the robustness test is to plot each parameter and model output against each other using the R function pairs(), Figure(7.8), which illustrates the strong correlations between parameters.

#robustSPM parameters against each other Fig 7.8

pairs(result[,c("r","K","Binit","MSY")],upper.panel=NULL,pch=1)

Figure 7.8: Plots of the relationships between parameters in the 100 optimum solutions stemming from fitting a surplus production model to the schaef data-set. The correlation between parameters is clear, although it needs emphasis that the proportional difference between estimates is very small being of the order of 0.2 - 0.3%.

7.3.3 Using Different Data?

The schaef data-set leads to a relatively robust outcome. Before moving on it would be enlightening to repeat the analysis using the dataspm data-set, which leads to more variable outcomes. Hopefully, such findings should encourage any future modellers reading this not to trust the first solution that a numerical optimizer presents.

#Now use the dataspm data-set, which is noisier

set.seed(777854) #other random seeds give different results

data(dataspm); fish <- dataspm #to generalize the code

param <- log(c(r=0.24,K=5174,Binit=2846,sigma=0.164))

ans <- fitSPM(pars=param,fish=fish,schaefer=TRUE,maxiter=1000,

funkone=TRUE)

out <- robustSPM(ans$estimate,fish,N=100,scaler=15, #making

verbose=FALSE,funkone=TRUE) #scaler=10 gives

result <- tail(out$results[,6:11],10) #16 sub-optimal results | r | K | Binit | sigma | -veLL | MSY | |

|---|---|---|---|---|---|---|

| 46 | 0.2425 | 5171.27 | 2844.29 | 0.1636 | -12.1288 | 313.537 |

| 77 | 0.2425 | 5171.51 | 2843.70 | 0.1636 | -12.1288 | 313.528 |

| 75 | 0.2425 | 5171.81 | 2846.73 | 0.1636 | -12.1288 | 313.545 |

| 79 | 0.2426 | 5169.36 | 2842.83 | 0.1636 | -12.1288 | 313.555 |

| 31 | 3.5610 | 149.62 | 50.74 | 0.2230 | -2.5244 | 133.201 |

| 65 | 0.0321 | 36059.56 | 49.72 | 0.2329 | -1.1783 | 289.163 |

| 60 | 40.3102 | 0.26 | 49.72 | 0.2329 | -1.1783 | 2.592 |

| 57 | 22.1938 | 0.00 | 49.72 | 0.2329 | -1.1783 | 0.016 |

| 38 | 1.1856 | 6062.64 | 49.72 | 0.2329 | -1.1783 | 1797.041 |

| 11 | 0.5954 | 4058.97 | 49.72 | 0.2329 | -1.1783 | 604.180 |

In those bottom six model fits with dataspm we can see cases of very large r values teamed with very small K values, very large K values teamed with small r values, and, in addition, in the last two rows, almost reasonable values for r and K, but very small Binit values.

7.4 Uncertainty

When we tested some model fits for how robust they were to initial conditions we found that when there were multiple parameters being fitted it was possible to obtain essentially the same numerical fit (to a given degree of precision) from slightly different parameter values. While the values did not tend to differ by much, this observation still confirms that when using numerical methods to estimate a set of parameters, the particular parameter values are not the only important outcome. We also need to know how precise those estimates are, we need to know about any uncertainty associated with their estimation. There are a number of approaches one can use to explore the uncertainty within a model fit. Here, using R, we will examine the implementation of four: 1) Likelihood profiles, 2) bootstrap resampling, 3) Asymptotic errors, and 4) Bayesian Posterior Distributions.

7.4.1 Likelihood Profiles

Likelihood profiles do what the name implies and provide insight into how the quality of a model fit might change if the parameters used were slightly different. A model is optimally fitted using maximum likelihood methods (minimization of the -ve log-likelihood), then, while fixing (keeping constant) one or more parameters to pre-determined values, one only fits the remaining unfixed parameters. In this way an optimum fit can be obtained while a given parameter or parameters have been given fixed values. Thus, we can determine how the total likelihood of the model fit will change when selected parameters remain fixed over an array of different values. A worked example should make the process clearer. We can use the abdat data-set, which provides for a reasonable fit to the observed data although leaving a moderate pattern in the residuals for the optimum fit and with relatively large final gradients on the optimum solution (try outfit(ans) to see the results).

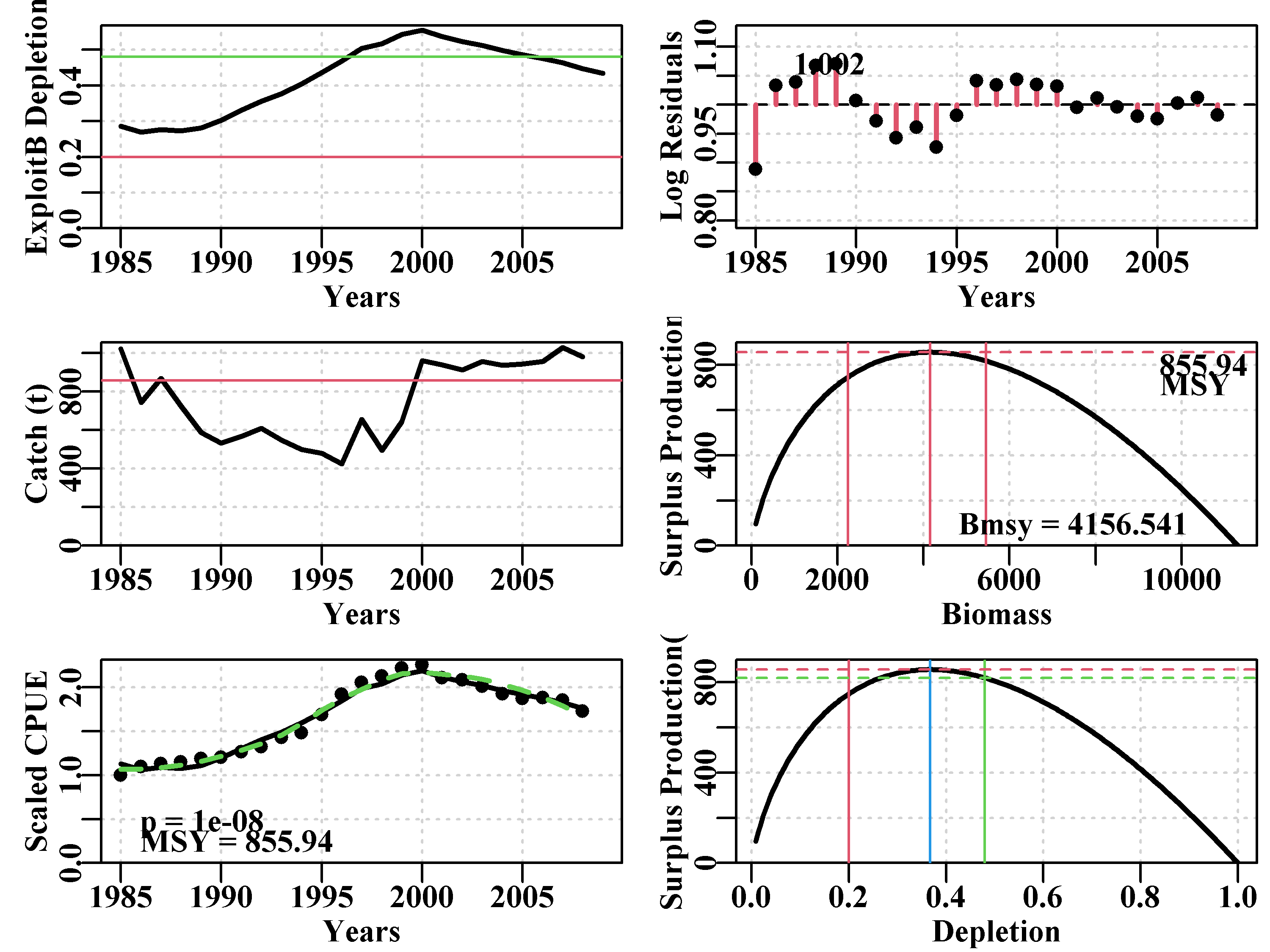

# Fig 7.9 Fit of optimum to the abdat data-set

data(abdat); fish <- as.matrix(abdat)

colnames(fish) <- tolower(colnames(fish)) # just in case

pars <- log(c(r=0.4,K=9400,Binit=3400,sigma=0.05))

ans <- fitSPM(pars,fish,schaefer=TRUE) #Schaefer

answer <- plotspmmod(ans$estimate,abdat,schaefer=TRUE,addrmse=TRUE)

Figure 7.9: Summary plot depicting the fit of the optimum parameters to the abdat data-set. The remaining pattern in the log-normal residuals between the fit and the cpue data are illustrated at the bottom right.

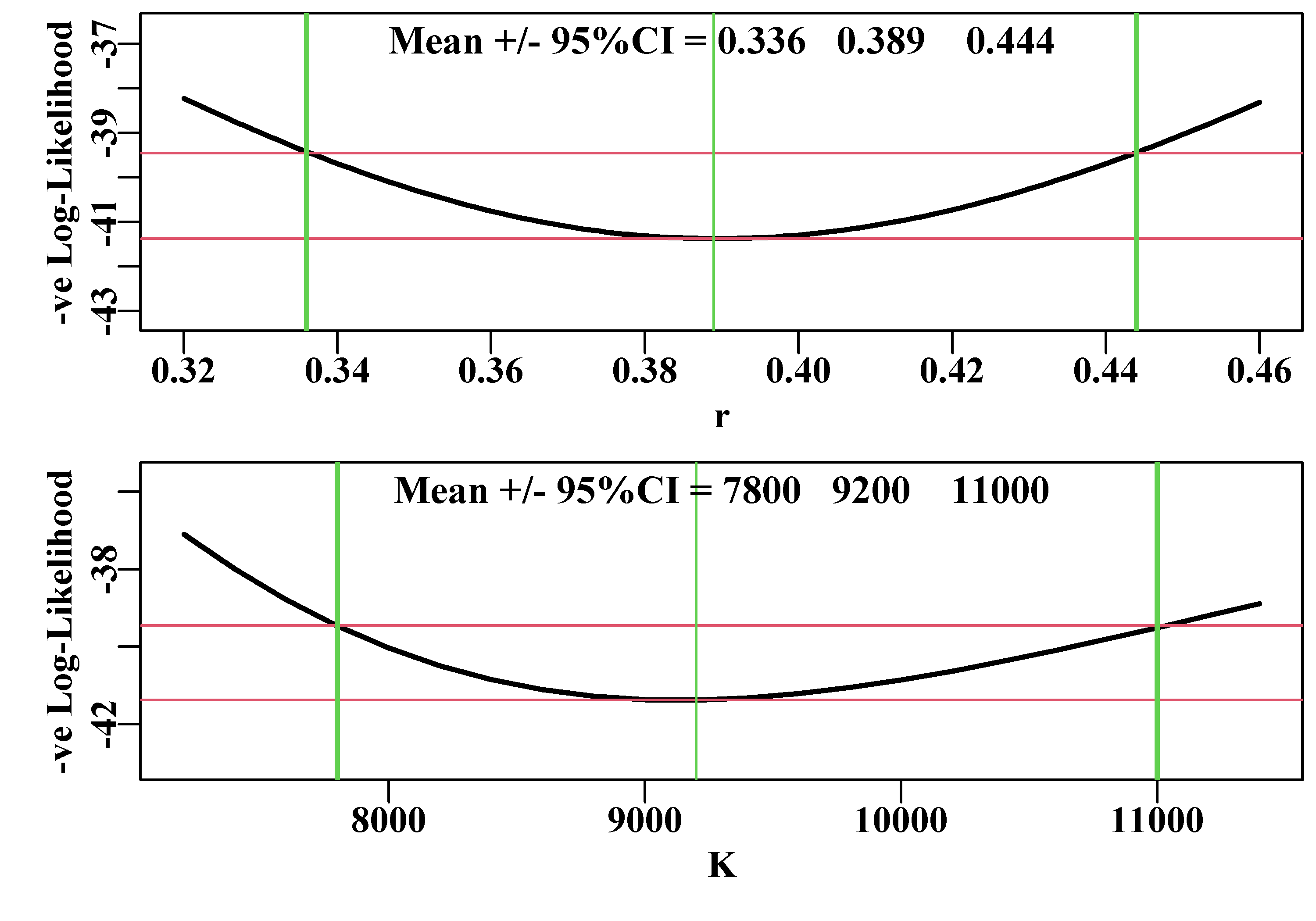

In the chapter On Uncertainty we examined a likelihood profile around a single parameter, here we will explore a little deeper to see some of the issues surrounding the use of likelihood profiles. We already have the optimal fit to the abdat data-set and we can use that as a starting point. If we consider the \(r\) and the \(K\) parameters in turn it becomes more efficient to write a simple function to conduct the profiles in each case to avoid duplicating code. As before we use the negLLP() function to enable some parameters to be fixed while others vary. As seen in the Uncertainty chapter, with one parameter the 95% confidence bounds are approximated by searching for the parameter range that encompasses the minimum log-likelihood plus half the chi-squared value for one degree of freedom (=1.92).

\[\begin{equation} {min(-LL)} + \frac{\chi _{1,1-\alpha }^{2}}{2} \tag{7.17} \end{equation}\]

When plotting each profile we can include this threshold to see where it intersects the likelihood profile, Figure(7.10).

# likelihood profiles for r and K for fit to abdat Fig 7.10

#doprofile input terms are vector of values, fixed parameter

#location, starting parameters, and free parameter locations.

#all other input are assumed to be in the calling environment

doprofile <- function(val,loc,startest,indat,notfix=c(2:4)) {

pname <- c("r","K","Binit","sigma","-veLL")

numv <- length(val)

outpar <- matrix(NA,nrow=numv,ncol=5,dimnames=list(val,pname))

for (i in 1:numv) { #

param <- log(startest) # reset the parameters

param[loc] <- log(val[i]) #insert new fixed value

parinit <- param # copy revised parameter vector

bestmod <- nlm(f=negLLP,p=param,funk=simpspm,initpar=parinit,

indat=indat,logobs=log(indat[,"cpue"]),

notfixed=notfix)

outpar[i,] <- c(exp(bestmod$estimate),bestmod$minimum)

}

return(outpar)

}

rval <- seq(0.32,0.46,0.001)

outr <- doprofile(rval,loc=1,startest=c(rval[1],11500,5000,0.25),

indat=fish,notfix=c(2:4))

Kval <- seq(7200,11500,200)

outk <- doprofile(Kval,loc=2,c(0.4,7200,6500,0.3),indat=fish,

notfix=c(1,3,4))

parset(plots=c(2,1),cex=0.85,outmargin=c(0.5,0.5,0,0))

plotprofile(outr,var="r",defpar=FALSE,lwd=2) #MQMF function

plotprofile(outk,var="K",defpar=FALSE,lwd=2)

Figure 7.10: Likelihood profiles for both the r and K parameters of the Schaefer model fit to the abdat data-set. The horizontal red lines separate the minimum -veLL from the likelihood value bounding the 95% confidence intervals. The vertical green lines intersect the minimum and the 95% CI. The numbers are the 95% CI surrounding the mean optimum value.

An issue with estimating such confidence bounds is that by only considering single parameters one is ignoring the inter-relationships and correlations between parameters, for which the Schaefer model is well known. But the strong correlation that is expected between the r and K parameters means that a square grid search obtained from combining the two separate individual searches along r and K will lead to many combinations that fall outside of even an approximate fit to the model. It is not impossible to create a two-dimensional likelihood profile (in fact a surface), or indeed a profile across even more parameters, but even two parameters usually requires carefully searching small parts of the surface at a time or other ways of dealing with some of the extremely poor model fits that would be obtained by a simplistic grid search.

Likelihood profiles across single parameters remain useful in situations where a stock assessment has one or more fixed value parameters. This will not happen with such simple models as the Schaefer surplus production model but such situations are not uncommon when dealing with more complex stock assessment models for stocks where biological parameters such as the natural mortality, the steepness of the stock-recruitment curve, and even growth parameters may not be known or are assumed to take the same values as related species. Once an optimum model fit is obtained in an assessment, within which some of the parameters take fixed values, it is possible to re-run the model fit while changing the assumed values for one of the fixed parameters to generate a likelihood profile for that parameter. In that way it is possible to see how consistent the model fit is with regard to the assumed values for the fixed parameters. Generating a likelihood profile in this manner is preferable to merely conducting sensitivity analyses in which we might vary such fixed parameters to a level above and a level below the assumed value to see the effect. Likelihood profiles provide a more detailed exploration of the sensitivity of the modelling to the individual parameters.

With regard to simpler models, such as we are dealing with here, there are other ways of examining the uncertainty inherent in the modelling that can attempt to take into account the correlations between parameters.

7.4.2 Bootstrap Confidence Intervals

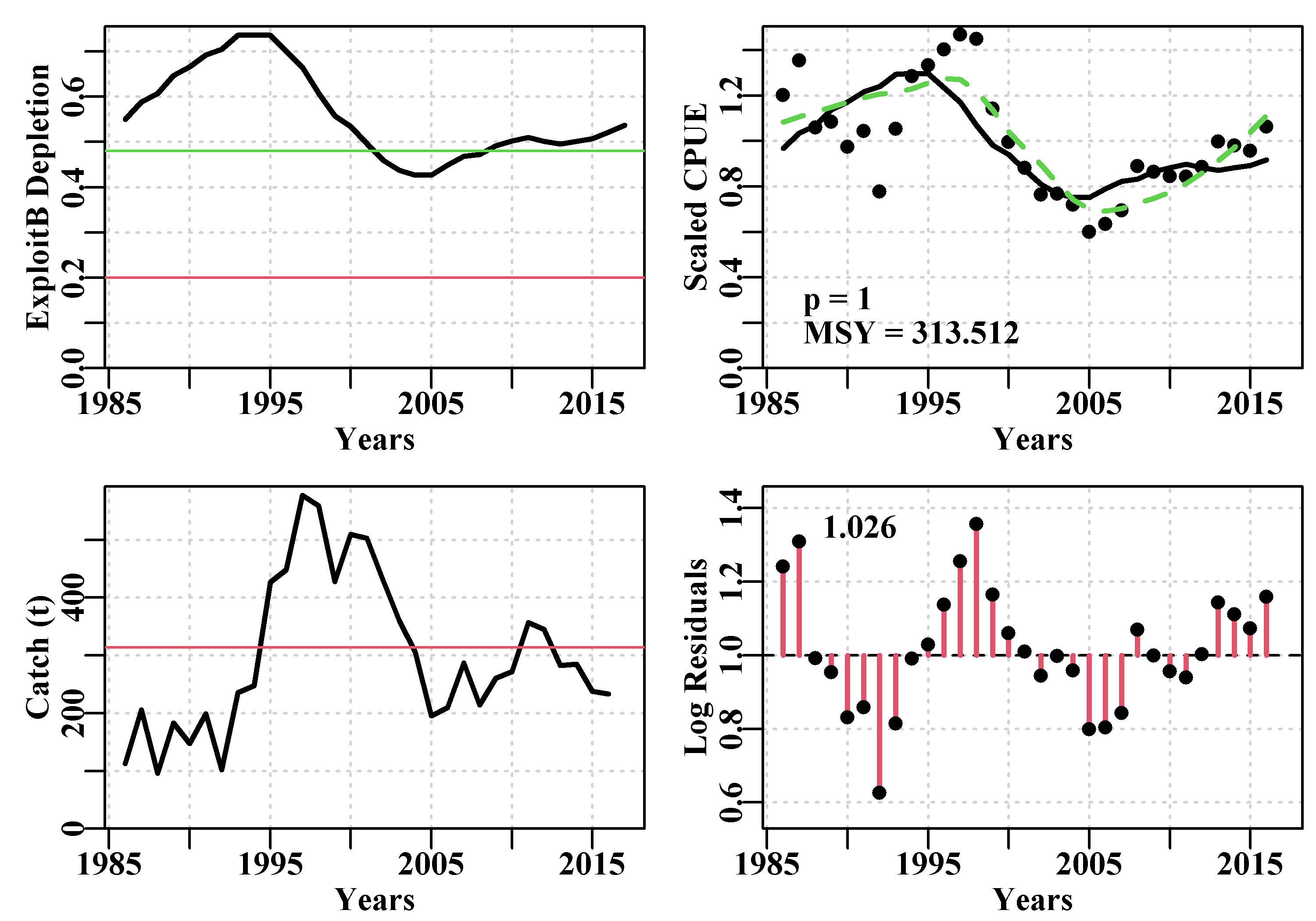

One way to characterize uncertainty in a model fit is to generate percentile confidence intervals around parameters and model outputs (MSY, etc) by taking bootstrap samples of the log-normal residuals associated with the cpue and using those to generate new bootstrap cpue samples with which to replace the original cpue time-series (Haddon, 2011). Each time such a bootstrap sample is made, the model is re-fit and the solutions stored for further analysis. To conduct such an analysis on surplus production models one can use the MQMF function spmboot(). Once we have found suitable starting parameters, we can use the fitSPM() function to obtain an optimum fit and it is the log-normal residuals associated with that optimum fit that are bootstrapped. Here we will use the relatively noisy dataspm data-set to illustrate these ideas

#find optimum Schaefer model fit to dataspm data-set Fig 7.11

data(dataspm)

fish <- as.matrix(dataspm)

colnames(fish) <- tolower(colnames(fish))

pars <- log(c(r=0.25,K=5500,Binit=3000,sigma=0.25))

ans <- fitSPM(pars,fish,schaefer=TRUE,maxiter=1000) #Schaefer

answer <- plotspmmod(ans$estimate,fish,schaefer=TRUE,addrmse=TRUE)

Figure 7.11: Summary plot depicting the fit of the optimum parameters to the dataspm data-set. The log-normal residuals between the fit and the cpue data are illustrated at the bottom right. These are what are bootstrapped and each bootstrap sample multiplied by the optimum predicted cpue time-series to obtain each bootstrap cpue time-series.

Once we have an optimum fit we can proceed to conduct a bootstrap analysis. One would usually run at least 1000 replicates, and often more, even though that might take a few minutes to complete. In this case, even in the optimum fit there is a pattern in the log-normal residuals, suggesting that the model structure is missing some approximately cyclic event affecting the fishery.

#bootstrap the log-normal residuals from optimum model fit

set.seed(210368)

reps <- 1000 # can take 10 sec on a large Desktop. Be patient

#startime <- Sys.time() # schaefer=TRUE is the default

boots <- spmboot(ans$estimate,fishery=fish,iter=reps)

#print(Sys.time() - startime) # how long did it take?

str(boots,max.level=1) # List of 2

# $ dynam : num [1:1000, 1:31, 1:5] 2846 3555 2459 3020 1865 ...

# ..- attr(*, "dimnames")=List of 3

# $ bootpar: num [1:1000, 1:8] 0.242 0.236 0.192 0.23 0.361 ...

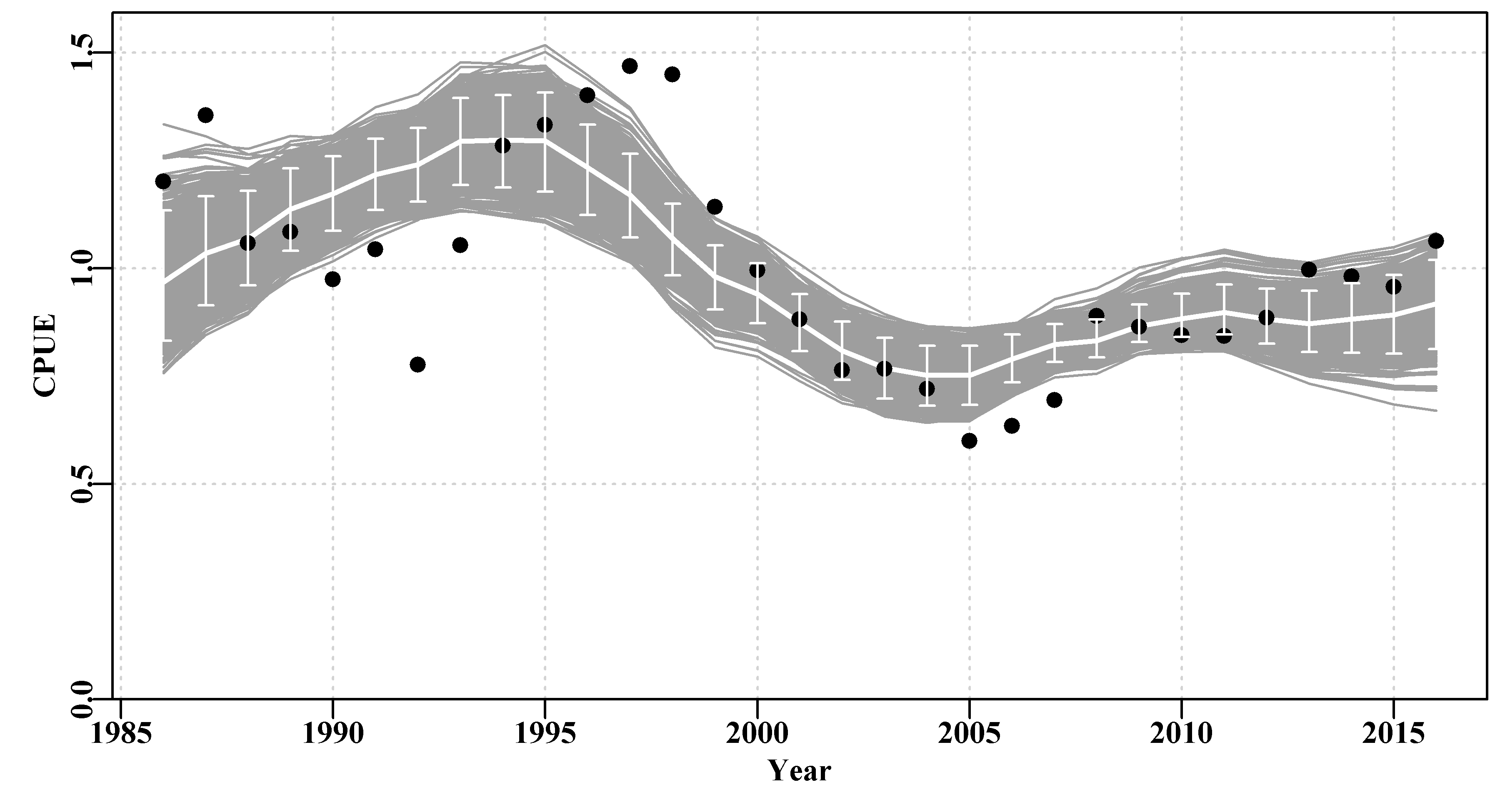

# ..- attr(*, "dimnames")=List of 2The output contains the dynamics of each run with the predicted model biomass, each bootstrap cpue sample, the predicted cpue for each bootstrap sample, the depletion time-series, and the annual harvest rate time-series (reps=1000 runs for 31 years with 5 variables stored). Each of these can be used to illustrate and summarize the outcomes and uncertainty within the analysis. Given the relatively large residuals in Figure(7.11) one might expect a relatively high degree of uncertainty, Table(7.5).

#Summarize bootstrapped parameter estimates as quantiles Table 7.6

bootpar <- boots$bootpar

rows <- colnames(bootpar)

columns <- c(c(0.025,0.05,0.5,0.95,0.975),"Mean")

bootCI <- matrix(NA,nrow=length(rows),ncol=length(columns),

dimnames=list(rows,columns))

for (i in 1:length(rows)) {

tmp <- bootpar[,i]

qtil <- quantile(tmp,probs=c(0.025,0.05,0.5,0.95,0.975),na.rm=TRUE)

bootCI[i,] <- c(qtil,mean(tmp,na.rm=TRUE))

} | 0.025 | 0.05 | 0.5 | 0.95 | 0.975 | Mean | |

|---|---|---|---|---|---|---|

| r | 0.1321 | 0.1494 | 0.2458 | 0.3540 | 0.3735 | 0.2484 |

| K | 3676.3569 | 3840.6961 | 5184.2237 | 7965.3318 | 8997.4945 | 5481.5140 |

| Binit | 1727.1976 | 1845.8458 | 2829.0085 | 4935.7516 | 5603.2871 | 3041.6876 |

| sigma | 0.1388 | 0.1423 | 0.1567 | 0.1626 | 0.1630 | 0.1551 |

| -veLL | -17.2319 | -16.4647 | -13.4785 | -12.3160 | -12.2377 | -13.8150 |

| MSY | 280.3701 | 289.4673 | 318.4197 | 352.7195 | 366.2422 | 319.5455 |

| Depl | 0.3384 | 0.3666 | 0.5286 | 0.6693 | 0.6992 | 0.5240 |

| Harv | 0.0508 | 0.0576 | 0.0877 | 0.1161 | 0.1236 | 0.0871 |

Such percentile confidence intervals can be visualized using histograms and including the respective selected percentile CI.

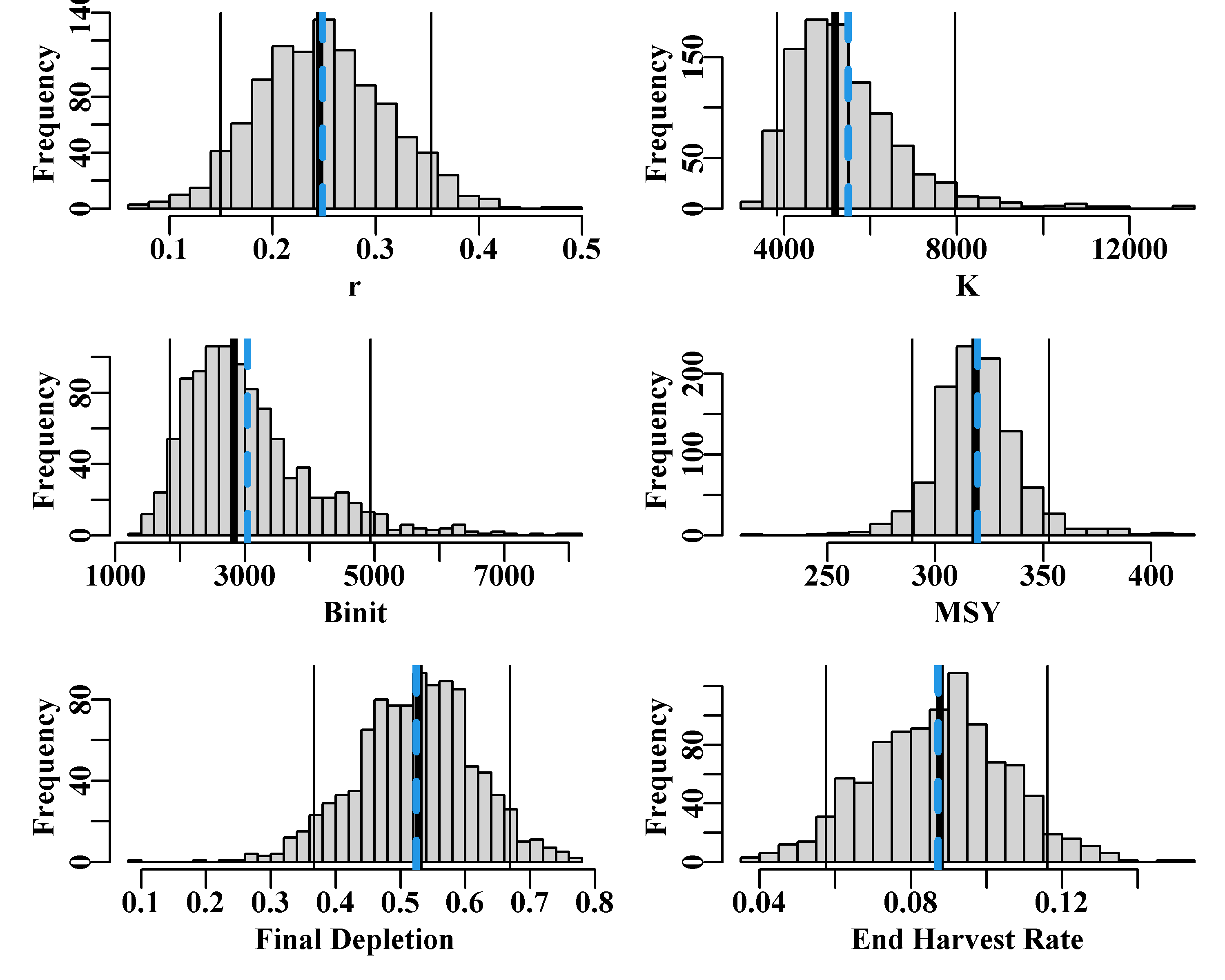

One would expect 1000 replicates would provide for a smooth response and representative confidence bounds but sometimes, especially with noisy data, one needs more replicates to obtain smooth representations of uncertainty. Taking 20 seconds for 2000 replicates might seem like a long time, but considering that such things used to take hours and even days, about 20 seconds is remarkable. Note that the confidence bounds are not necessarily symmetrical around either the mean or the median estimates. Notice also that with the final year depletion estimates the 5th percentile CI is well above \(0.2B_0\), implying that even though this analysis is uncertain the current depletion level is above the default limit reference point for biomass depletion used most everywhere with more than a 95% likelihood. We would need the central 80th percentiles to find the lower 10% bound, but it is bound to be higher than the 5th percentile. The medians and means exhibited by the K and the Binit values differ more than with the other parameters and model outputs, which suggests some evidence of bias, Figure(7.12). Because roughness remains in some plots these would be improved by increasing the number of replicates.

#boostrap CI. Note use of uphist to expand scale Fig 7.12

{colf <- c(1,1,1,4); lwdf <- c(1,3,1,3); ltyf <- c(1,1,1,2)

colsf <- c(2,3,4,6)

parset(plots=c(3,2))

hist(bootpar[,"r"],breaks=25,main="",xlab="r")

abline(v=c(bootCI["r",colsf]),col=colf,lwd=lwdf,lty=ltyf)

uphist(bootpar[,"K"],maxval=14000,breaks=25,main="",xlab="K")

abline(v=c(bootCI["K",colsf]),col=colf,lwd=lwdf,lty=ltyf)

hist(bootpar[,"Binit"],breaks=25,main="",xlab="Binit")

abline(v=c(bootCI["Binit",colsf]),col=colf,lwd=lwdf,lty=ltyf)

uphist(bootpar[,"MSY"],breaks=25,main="",xlab="MSY",maxval=450)

abline(v=c(bootCI["MSY",colsf]),col=colf,lwd=lwdf,lty=ltyf)

hist(bootpar[,"Depl"],breaks=25,main="",xlab="Final Depletion")

abline(v=c(bootCI["Depl",colsf]),col=colf,lwd=lwdf,lty=ltyf)

hist(bootpar[,"Harv"],breaks=25,main="",xlab="End Harvest Rate")

abline(v=c(bootCI["Harv",colsf]),col=colf,lwd=lwdf,lty=ltyf) }

Figure 7.12: The 1000 bootstrap replicates from the optimum spm fit to the dataspm data-set. The vertical lines, in each case, are the median and 90th percentile confidence intervals and the dashed vertical blue lines are the mean values. The function uphist() is used to expand the x-axis in K, Binit, and MSY.

The fitted trajectories, stored in boots$dynam can also provide a visual indication of the uncertainty surrounding the analysis.

#Fig7.13 1000 bootstrap trajectories for dataspm model fit

dynam <- boots$dynam

years <- fish[,"year"]

nyrs <- length(years)

parset()

ymax <- getmax(c(dynam[,,"predCE"],fish[,"cpue"]))

plot(fish[,"year"],fish[,"cpue"],type="n",ylim=c(0,ymax),

xlab="Year",ylab="CPUE",yaxs="i",panel.first = grid())

for (i in 1:reps) lines(years,dynam[i,,"predCE"],lwd=1,col=8)

lines(years,answer$Dynamics$outmat[1:nyrs,"predCE"],lwd=2,col=0)

points(years,fish[,"cpue"],cex=1.2,pch=16,col=1)

percs <- apply(dynam[,,"predCE"],2,quants)

arrows(x0=years,y0=percs["5%",],y1=percs["95%",],length=0.03,

angle=90,code=3,col=0)

Figure 7.13: A plot of the original observed CPUE (black dots), the optimum predicted CPUE (solid line), the 1000 bootstrap predicted CPUE (the grey lines), and the 90th percentile confidence intervals around those predicted values (the vertical bars).

There are clearly some deviations between the predicted and the observed CPUE values Figure(7.13), but the median estimates and the confidence bounds around them remain well defined.

Remember that whenever using a bootstrap on time-series data, where the values at time \(t+1\) are related to the values at time \(t\), it is necessary to bootstrap the residual values from any fitted model and relate them back to the optimum fitted values. With cpue data we are usually using log-normal residual errors so once the optimal solution is found those residual are defined as:

\[\begin{equation} \hat{I}_{t,resid} = \frac{I_t}{\hat{I_t}} \tag{7.18} \end{equation}\]

where \(I_t\) is the observed cpue in year \(t\), \({I_t}/{\hat{I_t}}\) is the observed divided by the predicted cpue in year \(t\) (the log-normal residual \(\hat{I}_{t,resid}\). There will be a time-series of such residuals and the bootstrap generation consists of randomly selecting values from the time-series, with replacement, so that a bootstrap sample of log-normal residuals is prepared. These are then multiplied by the original optimal predicted cpue values to generate different time-series of bootstrapped cpue.

\[\begin{equation} {I_t}^* = \hat{I_t} * \left [ \frac{I}{\hat{I}} \right ]^* \tag{7.19} \end{equation}\]

where the superscript \(*\) denotes a bootstrap sample, with \({I_t}^*\) denoting the bootstrap cpue sample for year \(t\), the \(\left [ \frac{I}{\hat{I}} \right ]^*\) denotes a single random sample from the log-normal residuals, which is then multiplied by the year’s predicted cpue. These equations reflect particular lines of code within the MQMF function spmboot().

A worthwhile exercise would be to repeat this analysis but everywhere schaefer = TRUE replace that with FALSE so as to fit the model using the Fox surplus production model. Then it would be possible to compare the uncertainty of the two models.

#Fit the Fox model to dataspm; note different parameters

pars <- log(c(r=0.15,K=6500,Binit=3000,sigma=0.20))

ansF <- fitSPM(pars,fish,schaefer=FALSE,maxiter=1000) #Fox version

bootsF <- spmboot(ansF$estimate,fishery=fish,iter=reps,schaefer=FALSE)

dynamF <- bootsF$dynam # bootstrap trajectories from both model fits Fig 7.14

parset()

ymax <- getmax(c(dynam[,,"predCE"],fish[,"cpue"]))

plot(fish[,"year"],fish[,"cpue"],type="n",ylim=c(0,ymax),

xlab="Year",ylab="CPUE",yaxs="i",panel.first = grid())

for (i in 1:reps) lines(years,dynamF[i,,"predCE"],lwd=1,col=1,lty=1)

for (i in 1:reps) lines(years,dynam[i,,"predCE"],lwd=1,col=8)

lines(years,answer$Dynamics$outmat[1:nyrs,"predCE"],lwd=2,col=0)

points(years,fish[,"cpue"],cex=1.1,pch=16,col=1)

percs <- apply(dynam[,,"predCE"],2,quants)

arrows(x0=years,y0=percs["5%",],y1=percs["95%",],length=0.03,

angle=90,code=3,col=0)

legend(1985,0.35,c("Schaefer","Fox"),col=c(8,1),bty="n",lwd=3)

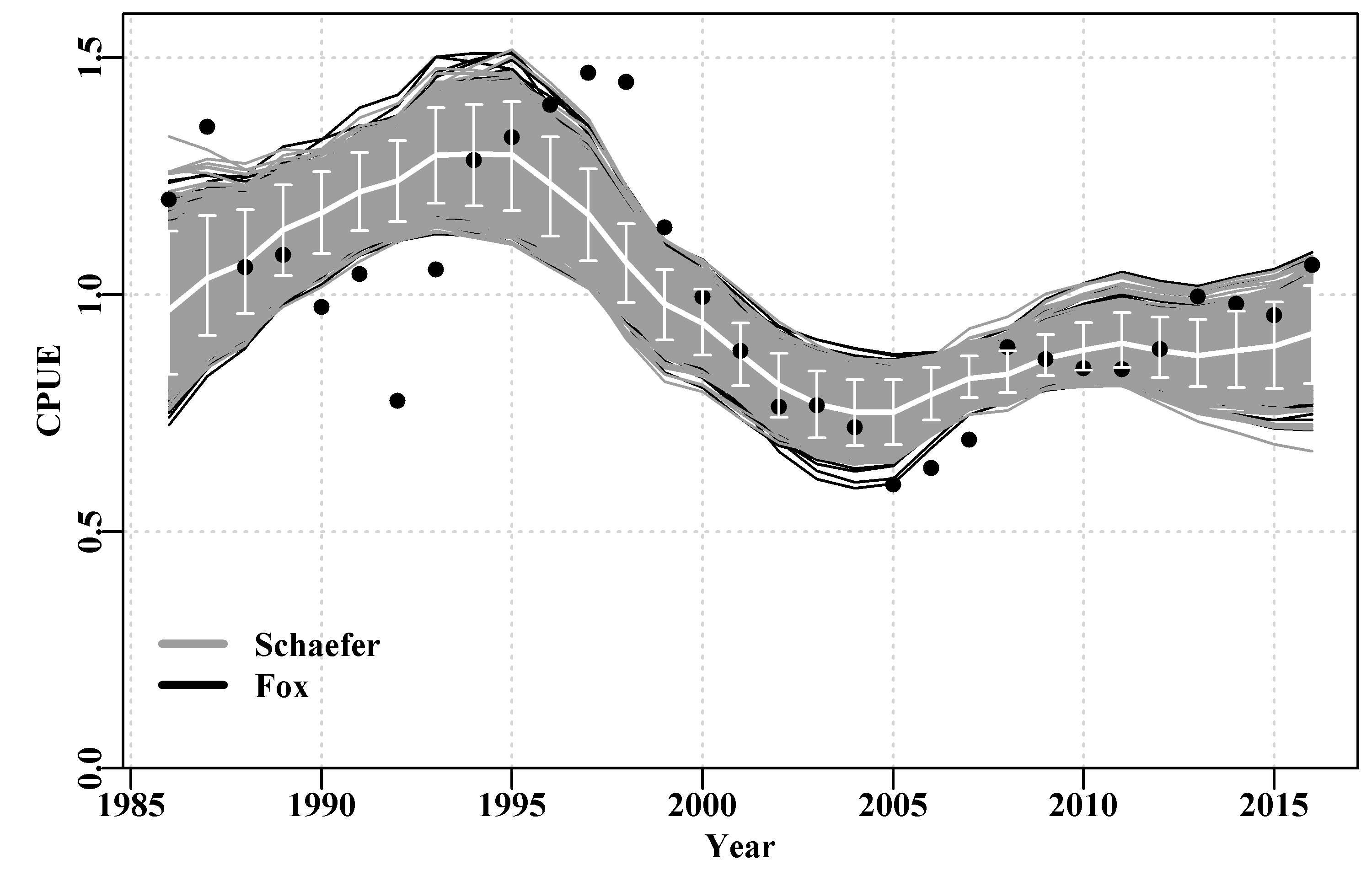

Figure 7.14: A plot of the original observed CPUE (dots), the optimum predicted CPUE (solid white line) with the 90th percentile confidence intervals (the white bars). The black lines are the Fox model bootstrap replicates while the grey lines over the black are those from the Schaefer model.

It could be argued that the Fox model is more successful at capturing the variability in this data as the spread of the black lines is slightly greater than that of the grey, Figure(7.14). Alternatively, it could be argued that the Fox model is less certain. Overall there is not a lot of difference between the outputs of the Schaefer and Fox models as even their predicted \(MSY\) values are very similar (313.512t vs 311.661t). However, in the end it appears the non-linearity in the density-dependence within the Fox model gives it more flexibility and hence it is able to capture the variability of the original data slightly better than the more rigid Schaefer model (hence its slighter smaller -ve log-likelihood, see outfit(ansF)). But neither model can capture the cyclic property exhibited in the residuals, which implies there is some process not being included in the modelled dynamics, a model misspecification. Neither model is completely adequate although either may provide a sufficient approximation to the dynamics that they could be used to generate management advice (with caveats about the cyclic process remaining the same through time, etc).

7.4.3 Parameter Correlations

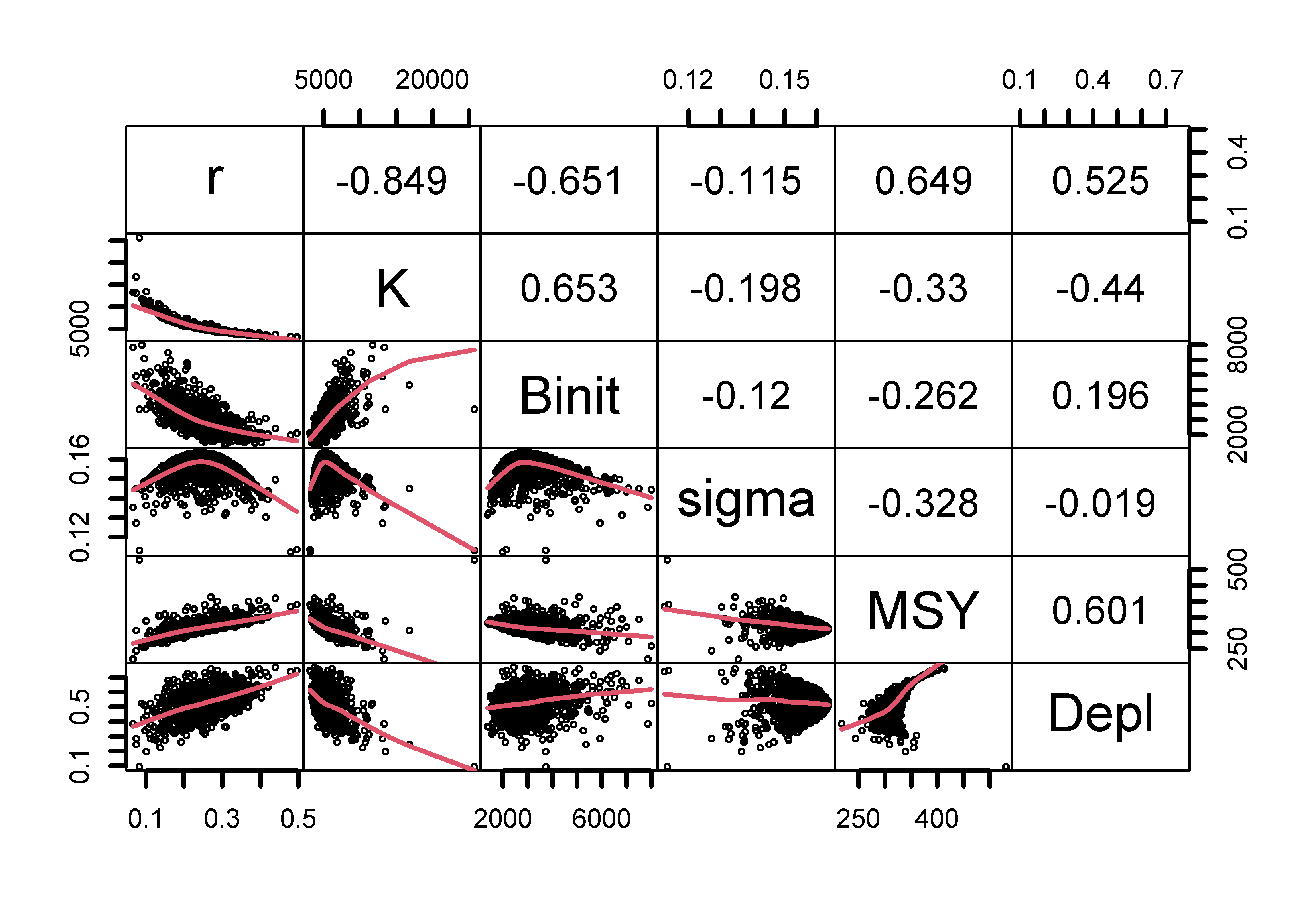

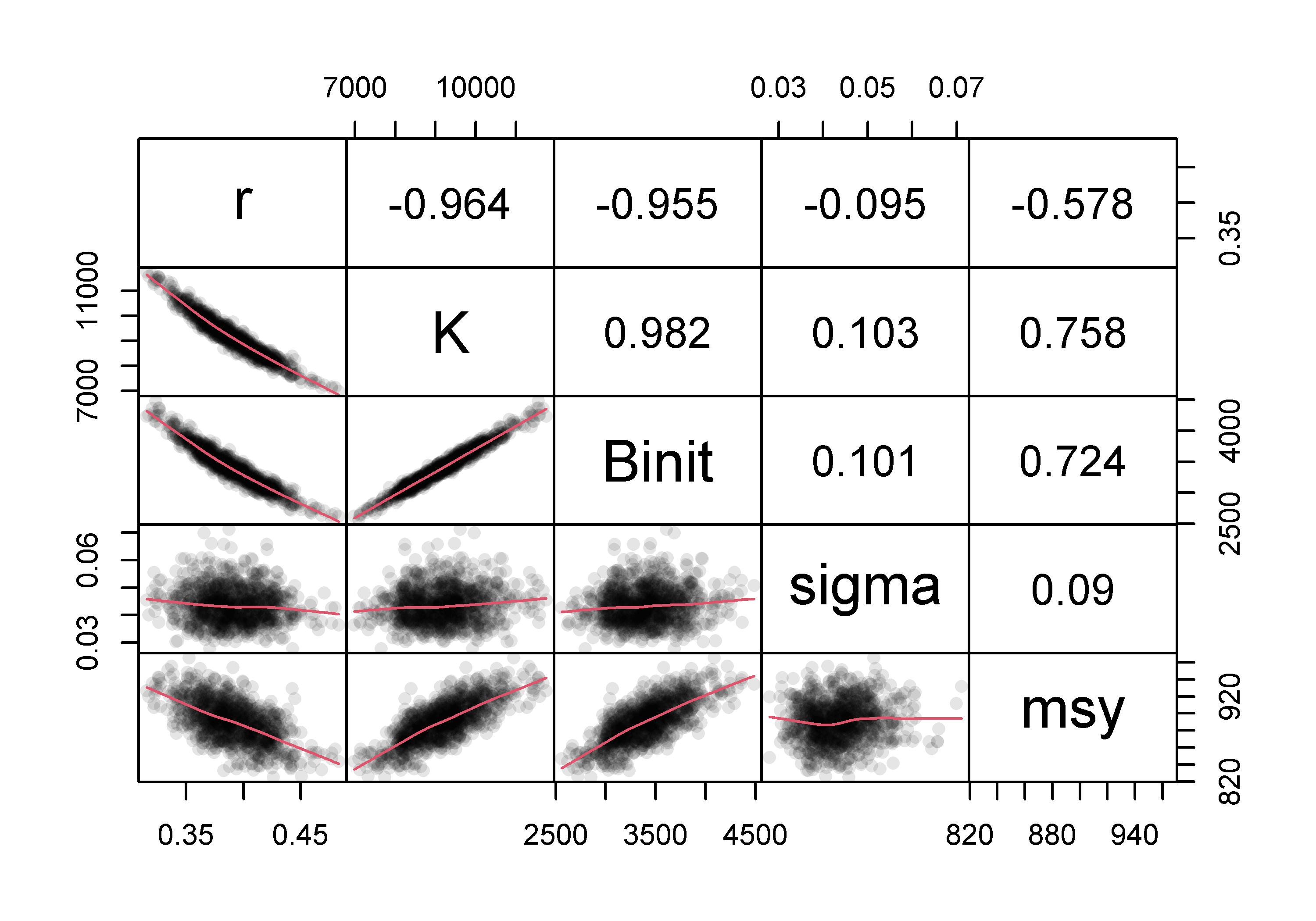

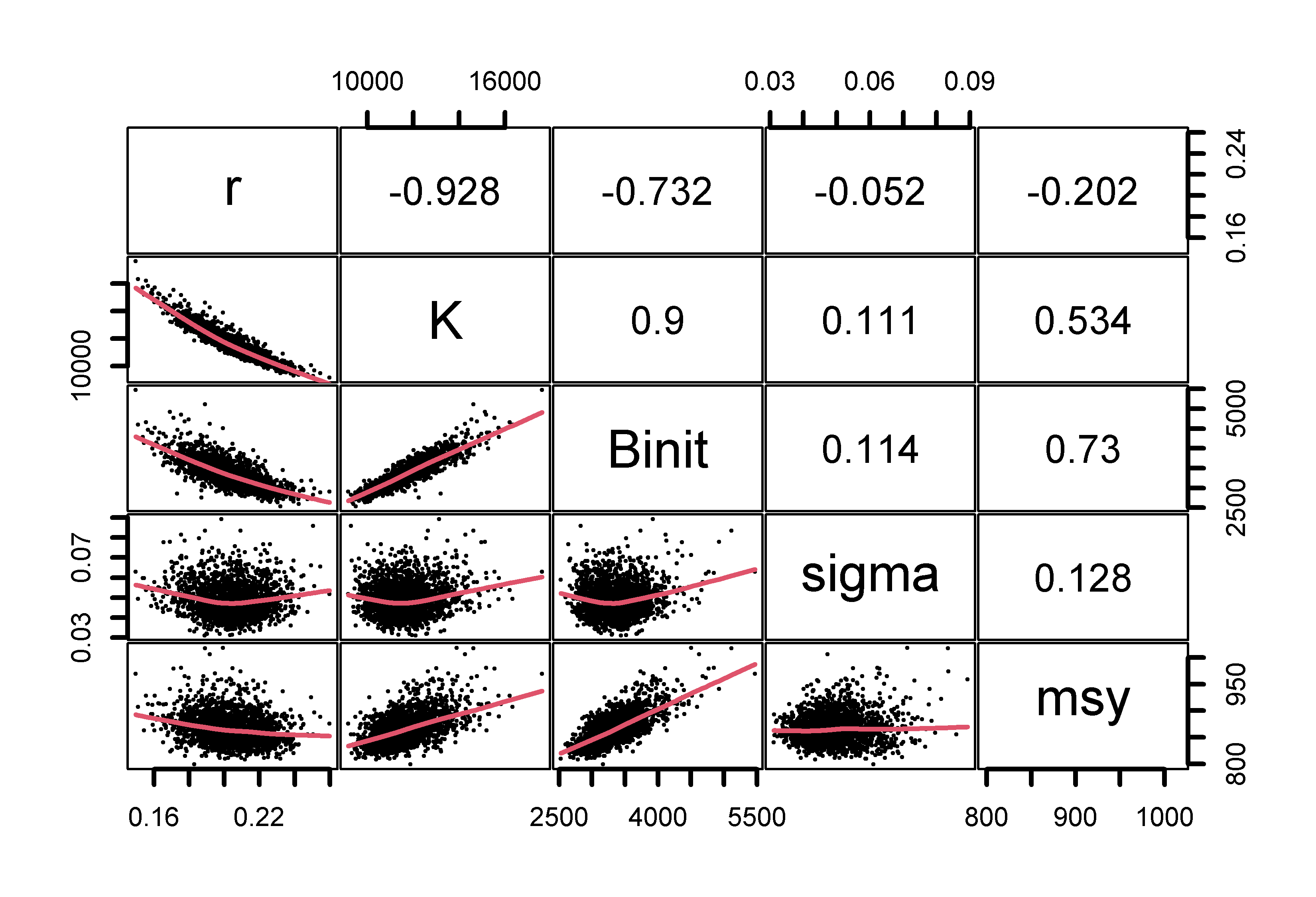

The combined bootstrap samples and associated estimates provide a characterization of the variability across the parameters reflecting both the data and the model being fitted. If we plot the various parameters against each other any parameter correlations become apparent. The strong negative curvi-linear relationship between \(r\) and \(K\) is very apparent, while the relationships with and between the other parameters are also neither random nor smoothly normal. There are some points at extreme values but they remain rare, nevertheless, the plots do illustrate the form of the variation within this analysis.

# plot variables against each other, use MQMF panel.cor Fig 7.15

pairs(boots$bootpar[,c(1:4,6,7)],lower.panel=panel.smooth,

upper.panel=panel.cor,gap=0,lwd=2,cex=0.5)

Figure 7.15: The relationships between the model parameters and some outputs for the Schaefer model (use bootsF$bootpar for the Fox model ). The lower panels have a red smoother line through the data illustrating any trends, while the upper panels have the linear correlation coefficient. The few extreme values distort the plots.

7.4.4 Asymptotic Errors

As described in the chapter On Uncertainty, a classical method of characterizing the uncertainty associated with the parameter estimates in a model fitting exercise is to use what are known as asymptotic errors. These derive from the variance-covariance matrix that can be used to describe the variability and interactions between the parameters of a model. In the section on the bootstrap it was possible to visualize the relationships between the parameters using the pairs() function and they were clearly not nicely multi-variate normal. Nevertheless, it remains possible to use the multi-variate normal derived from the variance-covariance matrix (vcov) to characterize a model’s uncertainty. We can estimate the vcov as an option when fitting a model using either optim() or nlm().

#Start the SPM analysis using asymptotic errors.

data(dataspm) # Note the use of hess=TRUE in call to fitSPM

fish <- as.matrix(dataspm) # using as.matrix for more speed

colnames(fish) <- tolower(colnames(fish)) # just in case

pars <- log(c(r=0.25,K=5200,Binit=2900,sigma=0.20))

ans <- fitSPM(pars,fish,schaefer=TRUE,maxiter=1000,hess=TRUE) We can see the outcome from fitting the Schaefer surplus production model to the dataspm data-set with the hess argument set to TRUE by using the outfit() function.

# nlm solution:

# minimum : -12.12879

# iterations : 2

# code : 2 >1 iterates in tolerance, probably solution

# par gradient transpar

# 1 -1.417080 0.0031126661 0.24242

# 2 8.551232 -0.0017992364 5173.12308

# 3 7.953564 -0.0009892147 2845.69834

# 4 -1.810225 -0.0021756288 0.16362

# hessian :

# [,1] [,2] [,3] [,4]

# [1,] 1338.3568627 1648.147068 -74.39814471 -0.14039276

# [2,] 1648.1470677 2076.777078 -115.32342460 -1.80063349

# [3,] -74.3981447 -115.323425 25.48912486 -0.01822396

# [4,] -0.1403928 -1.800633 -0.01822396 61.99195077The final minimization within fitSPM() uses maximum likelihood methods (actually the minimum negative log-likelihood) and so we need to invert the Hessian to obtain the variance-covariance matrix. The square-root of the diagonal also gives estimates of the standard error for each parameter (see chapter On Uncertainty).

#calculate the var-covar matrix and the st errors

vcov <- solve(ans$hessian) # calculate variance-covariance matrix

label <- c("r","K", "Binit","sigma")

colnames(vcov) <- label; rownames(vcov) <- label

outvcov <- rbind(vcov,sqrt(diag(vcov)))

rownames(outvcov) <- c(label,"StErr") | r | K | Binit | sigma | |

|---|---|---|---|---|

| r | 0.06676 | -0.05631 | -0.05991 | -0.00150 |

| K | -0.05631 | 0.04814 | 0.05344 | 0.00129 |

| Binit | -0.05991 | 0.05344 | 0.10615 | 0.00145 |

| sigma | -0.00150 | 0.00129 | 0.00145 | 0.01617 |

| StErr | 0.25838 | 0.21940 | 0.32581 | 0.12714 |